January 22, 2019

At Cornerstone, we believe that most investors should have a combination of both active and passive funds, but how do we decide where to utilize each style? Like all investment decisions we make, there are two conditions that need to be filled: first, does historical data support the rationale, and second, does the choice make common sense? Affirming the first question is not sufficient by itself, because with enough data, an earnest analyst can prove any thesis.

Using the following information from Callan Associates Inc.’s 3rd Quarter 2018 “Active vs. Passive Report” (“AVP”)[1] and quarterly peer group data allows us to quantitatively test where active management has added value in domestic equities. Callan’s median large cap mutual fund had a fee of 0.65% per year, whereas their average small cap manager charged fees of 0.91% per year. Over the past twenty years, the median large cap manager outperformed the S&P 500 by 0.18% per year before fees, whereas the median small cap manager bested the benchmark by 1.7% annually using the same metric. When adjusted for fees, the average large cap manager underperformed the benchmark by almost half a percent per year while the median small cap manager outperformed by 0.8% per year[2]. Thus, our first criterion indicates that investors should consider active management in small cap stocks but should passively manage large cap equities, all else being equal. Does this historical outcome make sense intuitively?

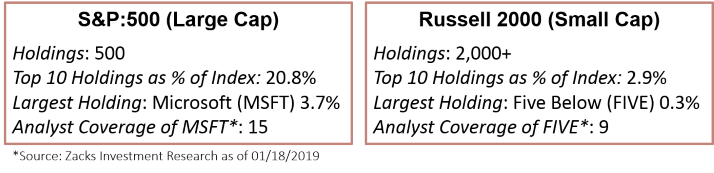

Looking at the chart above, active management in small cap stocks, again, seems logical. The S&P 500 is a widely analyzed, top-heavy index compared to small cap stock indexes, where there are fewer professionals covering a much broader investment universe. In short, it is less likely for a manager to have an informational advantage when it comes to Microsoft’s outlook versus that of Five Below, even though both are the largest stocks in their respective benchmarks. Even if information was the same between the two market caps, the S&P 500’s top ten holdings account for over 20% of the index versus only 3% in the Russell 2000. A small cap manager can choose to avoid a top holding of his benchmark with much less underperformance risk than can a manager of large cap stocks.

Jack Bogle’s vision, exemplified through the Vanguard platform, was to create cost effective investment vehicles for the masses. The pricing discipline that Vanguard forced upon the money management industry is rightfully admired. We do not believe that this means you must index your portfolio to achieve your outcomes. On the contrary, a good mix of passive investment with cost-conscious active management, properly allocated, can provide investors long-term benefits.

As always, we thank you for reading this edition of Independent Insights and look forward to your feedback. We are currently in the process of developing a similar piece put forth by our operations team, which you should be introduced to before the end of this month. We wish you all the best.

[1] Callan’s Active vs. Passive Report shows rolling 3-year returns versus benchmarks for the prior 20 years based on managers within their Performance Evaluation Program’s (“PEP”) database.

[2] All data referenced sourced from AVP and Callan’s 3Q 2018 PEP database.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.