August 5, 2020

“When you're in a hole, stop digging.”

The First Law of Holes

The US Census Bureau recently published a report that 30 million Americans faced food insecurity1 during the week ended July 21st. This problem is not solely COVID-19 related. It has existed for many years, but in the current uncertain times, how should we think about solutions to this and many other challenges we face? Any large-scale answer requires governmental and/or not-for-profit (“NFP”) support.

The federal government has stepped into the breach by trying to keep households and businesses afloat during this economic shutdown. Still, the desire to continue this role seems to be waning as we faced a fiscal cliff at the end of July when enhanced unemployment benefits were scheduled to lapse. We are still hopeful that some deal gets done to extend these for some period, but hope is not a strategy.

One legislative item on the books that can help is the CARES act, which allows taxpayers to make cash contributions to charitable organizations of $300 “above the line.” This is not adjusted in any way and can be used even if the taxpayer does not itemize. There are roughly 140 mm people who file tax returns in the US. If even one-fourth of them made this contribution, there would be $10.5 billion flowing into NFPs. That would not cure everything, but it certainly would be welcome.

The potential decline in governmental support leaves not-for-profit organizations to shoulder an even more massive load than they have traditionally. However, many charities have seen their revenue drop due to fewer fundraisers, less operating income, and falling endowment values. Increased demand (for charitable dollars) and decreased supply (of charitable dollars) is the challenge.

Recently, Pennsylvania enacted a law, Act No. 71 of 2020, which allows not-for-profits to dip deeper into their endowments than previous law allowed. The gist of the law is that instead of NFP’s being limited to spending no more than 7% of their average fair market value, for the next several years, they can spend 10% of the same. There were other tweaks to donor restrictions2, but our focus is on spending rate. (To see a piece, we recently published on spending policy considerations, please click here.)

It is apparent that, in some cases, taking advantage of the higher distribution rate will be necessary because there is no long-term survival for an organization that cannot endure the next several years. However, withdrawing 10% of the endowment’s value each year for the next three years establishes a Herculean required rate of return to maintain future purchasing power. So, what is a fiduciary at a charitable organization to do? One of the first steps we would suggest following that decision is to look at your endowment investments and make sure that the risk profile is not out of line with a fund being so heavily drawn upon.

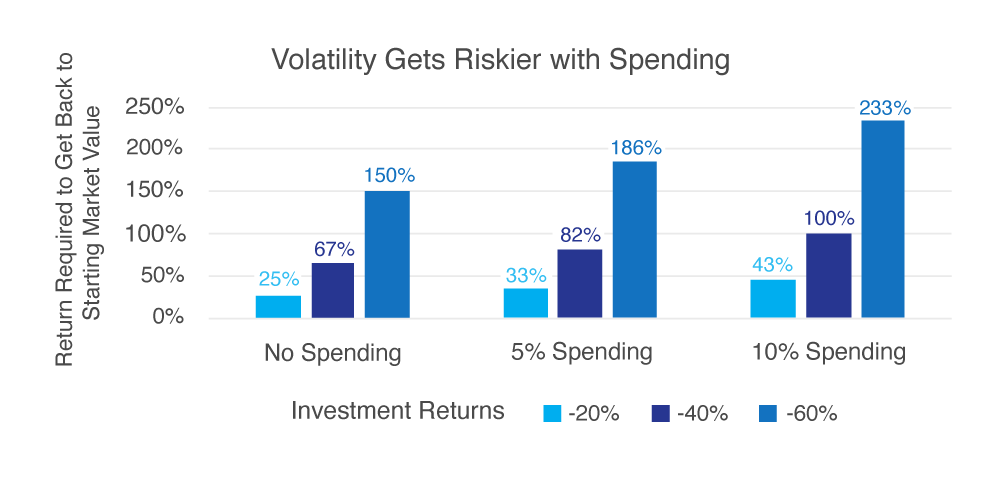

At first glance, it may seem that if the spending rate increases, the risk in the portfolio should also be dialed up to try and earn enough to maintain current asset levels; however, we would argue the opposite. As we have discussed in previous issues of Independent Insights, volatility is the friend of portfolios with inflows and the archnemesis of those with negative cashflows.

As the chart above shows, losses are punitive regardless of the level of spending but balloon when large losses are matched with high withdrawal rates. We describe this scenario as a vicious cycle. The flipside to this chart is that a fiduciary that removes too much of the risk from the portfolio is likely dooming it to also falling behind the eight-ball. We believe that the right level of risk is not universal. Each organization must weigh its needs and future outlook to optimize its portfolio; however, for that to happen, the fiduciaries must understand the risk they are taking on which requires higher-level performance measurement and risk assessment capabilities than many currently have at their disposal. The duty of the fiduciary is not to make the correct decisions, since many of them can only be known in retrospect, it is to make informed decisions.

Charitable institutions will not be saved purely by spending gimmicks. To believe so reminds us of the actuarial acrobatics that public pension funds have utilized over the years to kick the can down the road. What we need is a concerted effort by individuals and corporations to support these institutions in this time of need, to the extent they can. If a future gift is under consideration, speeding up the timeframe on that gift may help those running those institutions avoid having to make tough decisions that may weaken our charitable organizations, and therefore, our communities in the long run.

Perhaps the Second Law of Holes should be “when you’re in a hole, ask friends with buckets of dirt to show up.” As mentioned above, the CARES act provides a first step towards helping our charities. These are real, long term issues that we face, and we cannot rely on the government to have the fortitude to continue its support for the economy at the level it has been. We need our not-for-profit institutions to be able to provide support now without endangering their long-term viability. Our communities need healthy philanthropic organizations to thrive, but right now, those charities need their communities to survive.

1 Either sometimes or often not having enough to eat.

2 If you would like to read more on the changes to donor restrictions, you can visit Steven's & Lee's website here.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

Disclaimer Notice

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.