February 19, 2019

As of February 14, 2019, the United States’ federal debt was over $22 trillion and expected to grow by $1 trillion per year through 2022.[1] It appears everyone understands that the United States has a borrowing problem, but there is a divergence of opinions on what exactly that problem is. Some think we have borrowed too much, while recently some have argued that we are not indebted enough. The latter group consists of believers in Modern Monetary Theory (“MMT”.)

For most of its history, MMT has been a dispassionate accounting theory – private flows and public cashflows must sum to $0 absent inflation. However, for our purposes, we are using the recent political description: increasing public debt to fund social projects. According to MMT, government that can print its own money cannot go bankrupt. But what if there is not a limitless appetite for U.S. Treasury-backed debt?

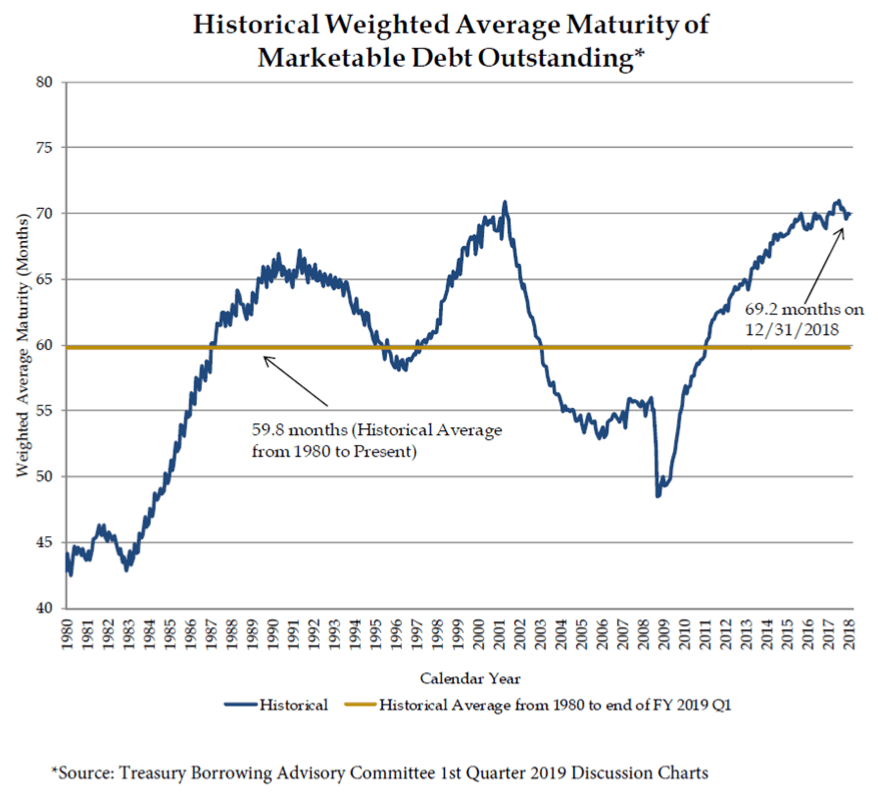

The chart above shows that the Treasury Department has extended the average maturity of its debt since the Great Recession. Unlike the previous examples of enterprises that failed because of a liquidity crunch, this maturity lengthening should provide a buffer for the government because it must refinance its debt less frequently. However, these numbers are skewed.

Since the advent of quantitative easing, a new funding source for our fiscal deficit has appeared: the Federal Reserve Board of Governors. The Fed currently owns 15% of our government’s total marketable debt and almost 30% of bonds due in ten or more years,[2] but it has also committed to eventually unwinding these positions. Given the coming surge in debt issuance, which will only be exacerbated if MMT becomes mainstream economics, will the government find willing buyers at reasonable terms, or will interest rates increase and cause an unsustainable debt cycle?

We often focus these pieces on short- to medium- term actionable items. This is not one of those times. We do not foresee demand drying up in the near term, but if, as a nation, we cannot pay down the principal outstanding, perhaps it is in our interest to control its growth. As always, thank you for reading along with us and please feel free to reach out with comments or suggestions.

[1] Source: United States Department of the Treasury and Office of Management and Budget estimates.

[2] Source: Board of Governors of the Federal Reserve System, “The Federal Reserve’s Balance Sheet” September 30, 2018.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.