January 7, 2020

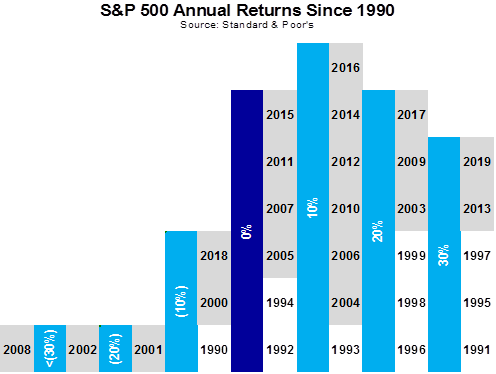

Even though it has been awhile since we have had such a banner year, the chart above shows that domestic equities have posted positive years 80% of the time since 1990. The average return of large cap stocks over that time is almost 11.5%, yet the compound growth rate (the amount by which an investment would have grown over that time) has only been 10%. That may not be intuitive without the knowledge that money grows geometrically – if you have a dollar and lose 50%, your remaining $0.50 must grow by 100% to get back to your original dollar. The same sad fact is true in the inverse – if your dollar increases by 100% to $2, you only need to lose 50% to get back to square one. The losses in 2001, 2002 and 2008 more than offset the years in which the market earned greater than 30% positive returns if an investor did not have money to buy more stocks during those dips.

What you will also notice about the graph above is that 1997 was followed by 2 years in which the S&P 500 had returns of more than 20%. While it is not our base expectation for 2020 and 2021 to repeat such strong performance, there are some similarities between today and 1997. Back then, a nascent technology, the internet, promised to increase the productivity of workers. Today, robotics, automation, and big data offer a similar path to increased economic activity. Back then, the Federal Reserve was becoming interventionist. Today, the Fed is solidly acting to promote economic growth. Back then, investors worried about heightened equity valuations that eventually spun up to unsustainable levels during the Tech Bubble. Today, investors are starting to talk about the market being “richly valued.” With investors facing few “cheap” alternatives to stocks, could we again see valuations spike? It is possible. We do not see the euphoria in the market today that was evident in the later 1990’s. As a matter of fact, we could make the argument that last year was one of the least loved market rallies in recent history. There is a lot of cash on the sidelines that could continue to fuel what is now the longest bull market in history.

Of course, if predicting markets was easy, we would all be sitting on a beach somewhere. The next decade will not likely look like the decade just passed, but long-term investors need to be in the risk asset game to earn positive real rates of return. At the same time, they need to be cognizant that large drawdowns can wipe away the good times quickly if they are not properly allocated.

We wish you and your families a wonderful New Year!

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.