June 25, 2019

“It is poor judgment to countersign another’s note, to become responsible for his debts.” - Proverbs 17:18

Homeownership has been a core component of the American dream since its founding. As such, the federal government has long supported policies promoting affordable housing financing. On this topic, we could rehash history: Fannie Mae and Freddie Mac, government sponsored entities (“GSEs”)[1], would have benefitted from better underwriting of the debts they were guaranteeing. [MC1] [YS2] We could also argue whether homeownership ranks as a public good deserving the use of our tax dollars (a political landmine conversation, if there ever was one), or discuss whether the bailouts of the GSEs were profitable for the government (yes they were, to the tune of over $100 billion after repayment of the loans[2]). Instead, we look to the future.There have been recent rumblings from the administration about removing the GSEs from the conservatorship of the Federal Home Financing Association (“FHFA”), which has overseen the two mortgage giants since the Great Recession. FHFA’s management of GSEs has elevated the guarantee that the federal government would backstop those debts from implicit to almost explicit levels.

There are obstacles to re-privatizing the GSEs, not the least of which is the fact that the government has been stripping profits from them for years, leaving their balance sheets obscenely leveraged without government support. Along with the need to recapitalize the lenders come other issues, such as what to do with current shareholders, how to manage these behemoths to avoid a repeat of past mistakes, and the fact that the Federal Reserve owns much of their debt.

There is also the matter of how private lenders can be involved in mortgage-backed securities issuance. Traditionally, banks have packaged their loans and sold them to the GSEs, who then turned them into bonds and guaranteed payments to investors. If the GSEs have neither an implicit guarantee from the government nor fortress-like balance sheets, why would a Wells Fargo, JPMorgan, etc. go to them as a middle man? If the market loses these intermediaries, how do investors decide on the investment quality of bank-issued bonds, and who polices mortgage rates?

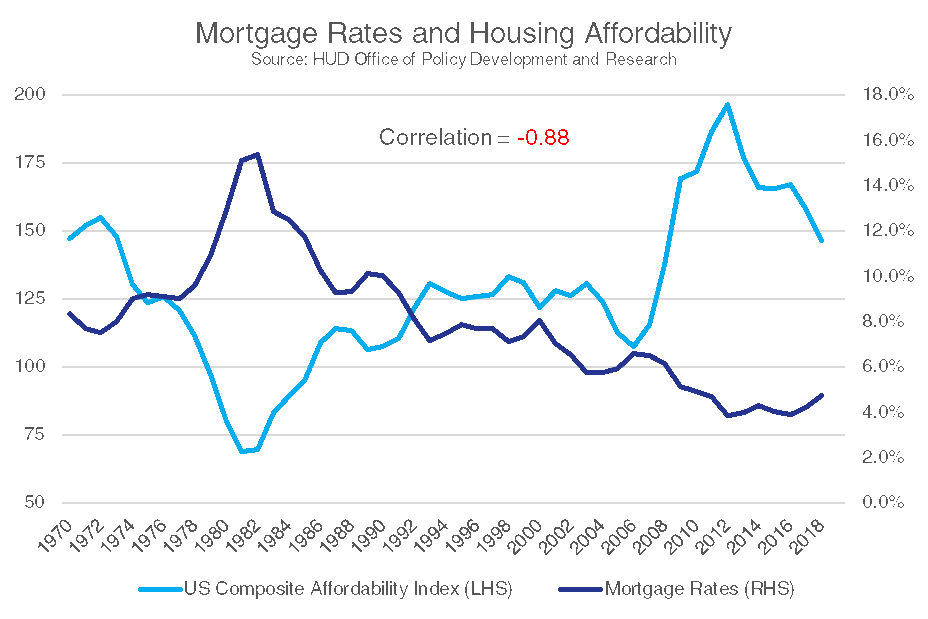

Measures of housing affordability looks at two inputs, the cost of housing and the cost of financing (i.e. the mortgage rate). The chart above shows that over the past 50 years there is an inverse correlation between affordability and mortgage rates. When one goes up, the other tends to go down and vice versa.

Investors should care about the pending changes for two reasons. First, if the mortgage market becomes more fragmented, it will become less liquid, raising the cost to both homeowners and investors alike. Secondly, according to the National Association of Homebuilders, 15-20% of the US economy is related to housing. As we learned back in 2008, housing issues spread quickly from Wall Street to Main Street.

As is our wont, we are discussing issues that may not come to fruition for some time but waiting until decisions are made to understand potential outcomes often is too late. The complexity and importance of the mortgage market, along with the fact that our Secretary of the Treasury, Steven Mnuchin does not support a disorderly privatization, allows us some measure of comfort.

Thanks for reading this edition of Independent Insights. We appreciate your support and feedback.

[1] For our purposes, the two GSEs are the Federal Home Loan Mortgage Corporation (“Freddie Mac”) and the Federal National Mortgage Association (“FNMA”). The Government National Mortgage Association (“Ginnie Mae”) is a GSE but is backed explicitly by the federal government and did not require assistance during the financial crisis.

[2] Source: Federal Housing Finance Agency Tables 1 & 2 as of Q1 2019

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

Disclaimer Notice

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.