June 28, 2022

History has no shortage of famous investors. Apple in the 1980’s was not a part of famed value investor Warren Buffet’s portfolio, yet it makes up over 40% of Berkshire Hathaway’s public holdings at the time of this writing. Disruptive innovation investor Cathie Wood, the CEO of Ark Invest, prefers a bumpier ride, often seeking non-profitable companies growing at exponentially high rates. Her hope is to catch a handful of winners that disrupt traditional industries and become dominant in the new economy. Carl Icahn’s investment compass led him to finding mismanaged companies he could invest in and change through shareholder activism. If they came out better, Icahn profited handsomely. Put simply, different investors apply their innate investment compasses to guide their long-term investment path.

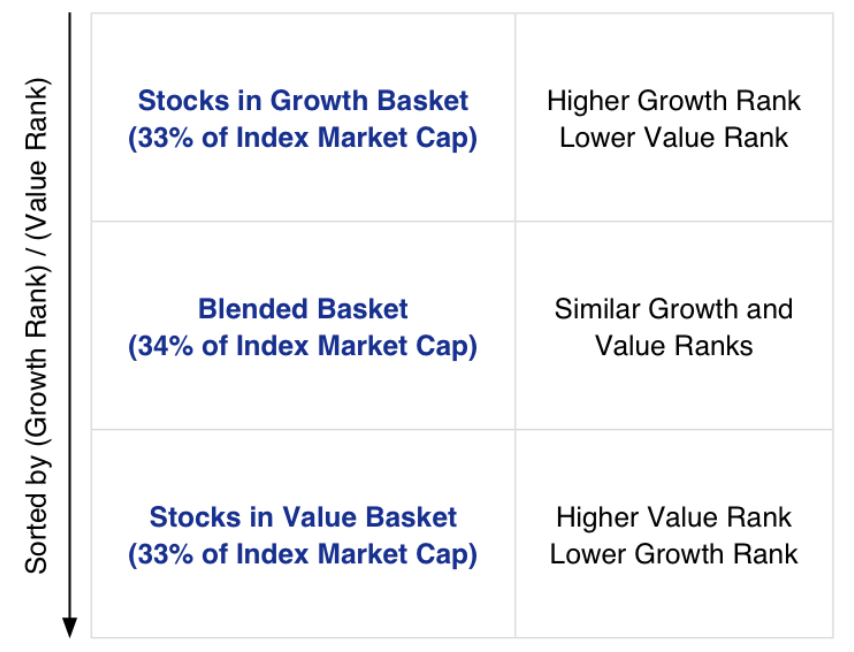

How does one find their true north for investing and choose managers for their investment portfolio?An investor can distill a large universe of stocks by following their own investment compasses. For instance, income investors screen for dividend paying stocks and then conduct fundamental research on each to discern which make sense. Low volatility investors might screen for high quality stocks and then take extra time to seek which names align with their investment thesis. Some of the oldest and broadest factors are growth and value. Growth and value are a continuum, with some stocks exhibiting severe value traits while others produce extreme growth. Of course, there is a whole universe of options in-between. For the sake of simplicity, we will define growth and value using index provider Standard & Poors (S&P) methodology.

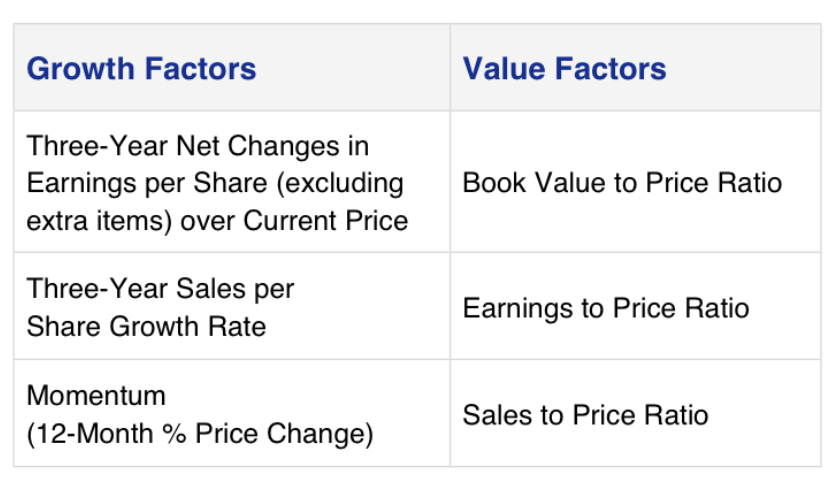

S&P uses three measures or factors to define growth and value.

By this definition, growth stocks will have high earnings-per-share, high sales growth, and strong upward price momentum. Value stocks will have high book, earnings and sales-to-price characteristics. Rates of growth are more prized in the growth bucket, whereas earnings levels are more prized the value bucket. This methodology is known as a pure interpretation. There is no overlapping of names between the buckets. Other index providers use various weighting schemes that allow for some stock overlap and re-weight according to their scoring methodologies.

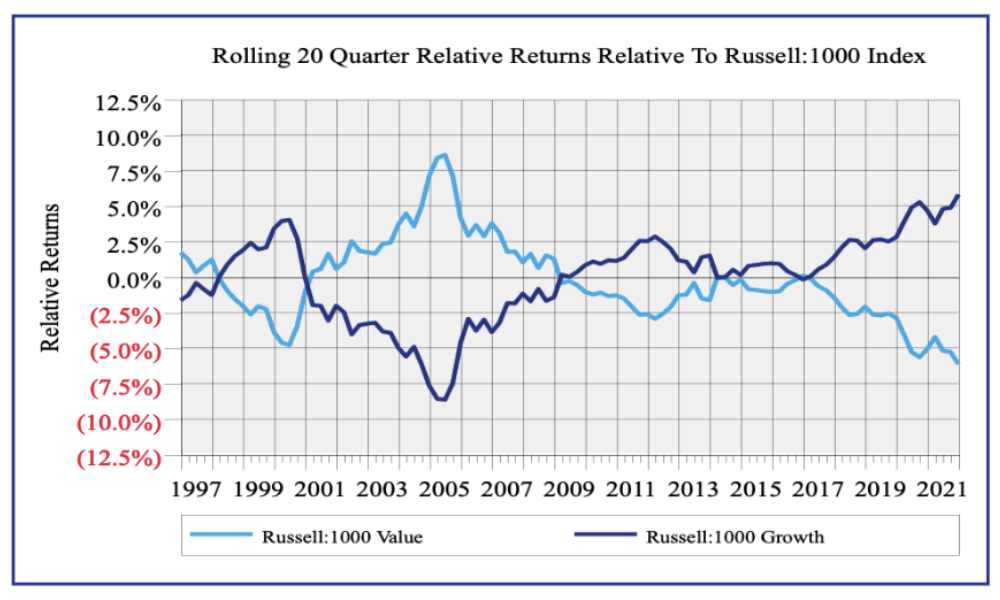

What works best? It depends. Growth and value tend to go in and out of favor with investors. When economic uncertainty is high, having dependable, real earnings today may lead value to outperform – except during the COVID-19 pandemic when growth stocks outperformed. When the economy is booming, one might think growth-centric names should command higher prices – except during the mid-2000’s when value stocks outperformed. The truth is, predicting the future is hard, and the correlations between short-term economic performance and stock market performance are shaky at best.

If growth and value styles go in and out of favor, why not just pick a blend of both? You should, but don’t totally abandon the extremes. Selecting a blended equity manager may seem like the easy solution to a comfortable performance ride, except it limits the opportunity set and the advantages of specialization.

There are a few problems with the traditional active, blended equity manager as well.

- Few utilize a balanced, middle approach. Most lean toward the growth or value ends of the spectrum

- Some analysts neglect deep value or high growth names, they limit their universe because they lack a thorough understanding of those areas

- Many analysts follow names that exhibit similar growth and value characteristics making it hard for an investor to gain an informational advantage

Growth and value managers have their own problems. They can know a stock so well they become biased. They can also avoid some mainstream names with durable businesses that exhibit both growth and value factors. Nobody is perfect so we blend styles into aggregate portfolios. Equity buckets have passive and active management with growth and value styles represented. Fixed income sleeves have core, core plus, and short duration bond managers. Alternative baskets have various underlying strategies with lower correlations to traditional equities and fixed income.

Remember those famous investors? They got famous by applying a specific investment style over long periods of time. They all suffered performance woes at some point in their careers – Cathie Wood seems to be having her moment as we speak. However, each of those famous investors achieved success by patiently and consistently applying their investment philosophy; seeking their true north.

By definition, a diversified portfolio should have managers who are in favor and others who are out of favor at any given point in time. If everyone is going in the same direction, there is likely a large bet in the portfolio you should consider. By blending various investment strategies and styles, we believe we can increase the chances of our managers in adding value (out-performance) to portfolios, often with less risk. This is not an achievable goal in any given quarter or year, but something we strive for over full market cycles.

Investors usually achieve fame by making large market calls or bets. We recognize the value of that strategy, however, we prefer having many investors making lots of diversified bets on a smaller scale within our portfolios to achieve success for our clients. Our portfolio construction philosophy aims to smooth the investment performance experience so that we can remain invested through not only well-behaving markets, but also through difficult ones so that we may realize long term success.

Past performance is no guarantee of future results. Securities offered through M Holdings Securities, Inc., a Registered Broker/Dealer, Member FINRA/SIPC. Investment Advisory Services offered through Cornerstone Advisors Asset Management, LLC, which is independently owned and operated.This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of June 2022 and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.