September 2, 2021

Recently Brian Bobeck, who runs our life insurance operation, came to our analyst team with a project. To paraphrase, it went like this:

“I have a client who owns a business and knows that he needs insurance. He wants to buy a no-lapse-guarantee (”NLG”) product[1], but given his circumstances, I think he’s overpaying for that compared to what he could buy using a variable universal life (“VUL”) policy.”

Far from being experts at life insurance products (we leave that to our very capable insurance team), our analysts thought that a breakeven analysis was in order, so we asked what a variable policy would have to earn to have a similar outcome to an NLG alternative. This would at least approximate the true cost of the NLG rider.

We learned by analyzing some insurance illustrations with our insurance team that the breakeven rate between the two types of policies was under 4%, given a particular funding strategy. Since future capital markets’ performance are unknown, we rounded that to 4%.

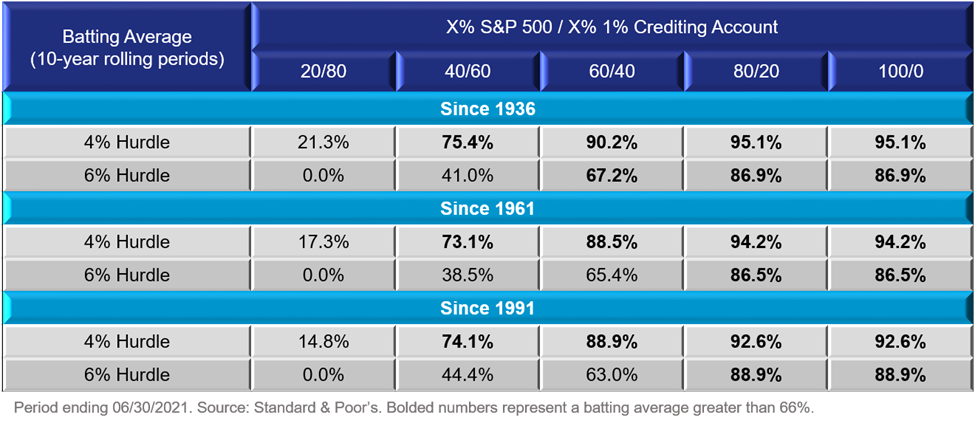

Here are some notes on our process before getting into the output:

- Instead of overengineering the analysis, we assumed that there were only two investments (the S&P 500 and a fixed rate account.) VUL policies offer many investment options, but we felt that complicating the portfolio would do little to advance the conversation.

- If you have sat through our capital markets expectation presentation, you know that our outlook for bonds over the next decade is significantly lower than they have performed historically. Thus, instead of using historical bond returns to give a boost to VUL performance, we thought a fixed account paying 1% per year was more appropriate.

- We ran the analysis with various weightings between the S&P 500 and the fixed account. We did not include an all fixed portfolio because we knew that would also fail to meet the hurdle rate.

- For simplicity’s sake and to increase our number of observation periods, we looked at 10-year rolling returns of the asset mixes over different time periods through June 30, 2021 (from 1936, from 1961, and from 1991.)

- Even though we already increased the assumed required rate of return of the variable policy to 4%, we understand that there is some price that investors are willing to pay for peace of mind (NLGs are set it and forget it as long as you make your payments.) We also ran our analysis with a heightened hurdle rate of 6% to account for that behavioral finance preference for safety.

- “Batting Average” is the percentage of time that a portfolio has outperformed a specified return and/or benchmark. In this case, the numbers below are the percent of rolling periods in which the portfolio mix outperformed the hurdle rate.

The output of the analysis is both compelling and intuitive. If the investor is unwilling to allocate enough of the assets to the stock market, the NLG product dominates the VUL. In that case, the cost of the policy owner’s peace of mind is extremely high. Increasing the risk of the underlying investment portfolio greatly improves the batting average and one might even say dominates the hurdle rates. Interestingly, an investor does not increase his chances of success by going all into risk assets as 80/20 models hit the hurdle rates at the same percentage as 100% portfolios.

There are many intricacies to life insurance that we have not covered here, but a market participant who is not extremely bearish on the capital markets would have achieved better outcomes in most scenarios by foregoing the promises of the insurance company and instead embracing the uncertainties of the financial markets.

This is a specific case for a specific client, but these situations are not uncommon. In fact, investors face them every day. Think about the 40-year-old who has saved prudently for retirement but is wary of the future of the stock market. She has another four or more decades in which to save and then live off of those savings. Depending on the amount of fear she feels, the allure of a money market which will not lose money can be strong. But what is she potentially giving up? What about the investment committee of an endowment that focuses too heavily on maintaining their current spending and therefore maintains a risk-averse portfolio? For many, avoiding financial risk is human nature, but doing so also comes with costs.

My apologies for it having been so long since the last issue of Independent Insights. We will be back in the swing of things and look forward to sharing more of our thoughts soon. Be well and stay safe. Thank you, as always, for taking the time to read this. We would love to hear thoughts, comments or ideas for future notes.

[1] The specifics of these policies is not important to our findings other than the NLG product will pay a death benefit up to a certain age if premiums are paid as scheduled, but a VUL policy relies on the performance of an underlying investment portfolio to stay in force. If you have any questions or life insurance needs, please reach out to Brian and his team at bbobeck@cornerstone-companies.com.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.