March 17, 2021

A colleague of ours prepares a weekly internal report that provides us with a snapshot of the performance of various bellwether indexes and fund managers. It allows us to see how different sectors are faring over various periods. Sometimes, though, it can also serve as a reminder of how fickle endpoint sensitivity can be in the financial markets.

On March 23, 2020, the Russell 1000 Value had bottomed out. It was down over 37% year-to-date due to the pandemic and economic shutdown. Flash forward almost a year, and the same benchmark finished 2020 with a positive return and was up over 10% for 2021 through March 11, 2021. For a rolling one-year period, as of the same date, the same benchmark has gained almost 43%. Small-cap stocks have exhibited larger gyrations. The Russell 2000 has a chance of earning a 100% return in a one-year period before the last of 2020’s bear market is rolled off later this month.

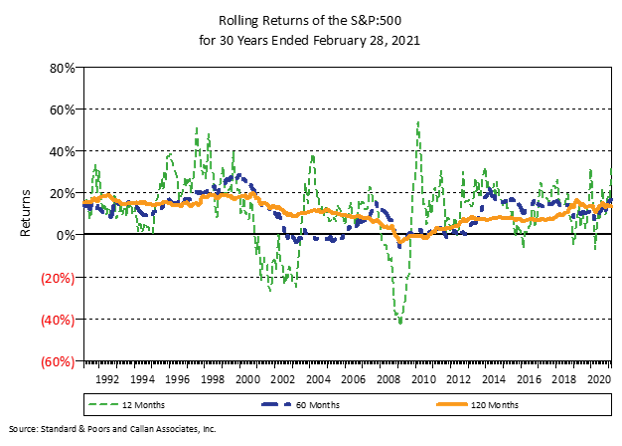

We chose an extreme time period to prove a point, but it is an important one for investors to remember. As the chart above shows, over short periods of time, the market has exhibited severe undulations, but as one stretches the time period, the variations become much smaller. For example, when looking at twelve-month rolling periods, the market has dropped more than 20% several times and gained greater than 40% a handful of times since the early 1990s. For five-year periods, the highs and lows moderate significantly, and over 10-year rolling periods, the market rarely has had a negative return but also has not posted annualized returns significantly over 20% for a decade in the modern era.

You may ask why we share this information with you now. The market has been favorable for a year and for the most part has trended upwards since the rebound from the Great Recession in 2008. But remember back 12 months, and you may not have been as optimistic about the market recovery. We do not blame you. It is stressful to look at your account when it is losing money. In the midst of a freefall, it is not easy to take a step back for perspective. Bear markets often happen when the world seems the most out of control. It feels right to do something, anything, to feel like you are in command. When that feeling occurs is when we suggest investors unplug and make no decisions of significance. Emotional decisions on either end of the risk spectrum can lead to regretful outcomes.

The period to plan for the next market reversal is now when markets are back near all-time highs, not after they have suffered significant losses. It is less mentally taxing to align your portfolio with your investment horizon when markets are strong. If you have already sat with us to review our capital market assumptions for the next decade, you have done the hard part of visualizing what poor capital markets can do to your portfolio. If you have not, consider how you would react to another drawdown like last year. Given enough time, it will happen again. If it took a team of horses to prevent you from reacting during the panic of last March, perhaps you consider making changes now, but what we have found is that investment portfolios can often weather market volatility better than the psyche of the investors responsible for them. If given the chance, the portfolio can recover losses over time. Time allows the miracle of compound interest to take hold and enhance wealth. If your current portfolio is aligned with your needs, the next time you find your stomach churning from the rollercoaster that is short-term market dynamics, you should mentally mosey on over to the treadmill of long-term results. It may not be as exhilarating, but it can keep you and your portfolio on a healthy path.

These articles may sometimes sound like broken records. Yet, some rules that are crucially important are also incredibly easy to forget under stress. If you would like to discuss your portfolio or know someone who would benefit from talking with us, we would welcome the conversation. We hope you are doing well and looking forward to Spring.

On March 23, 2020, the Russell 1000 Value had bottomed out. It was down over 37% year-to-date due to the pandemic and economic shutdown. Flash forward almost a year, and the same benchmark finished 2020 with a positive return and was up over 10% for 2021 through March 11, 2021. For a rolling one-year period, as of the same date, the same benchmark has gained almost 43%. Small-cap stocks have exhibited larger gyrations. The Russell 2000 has a chance of earning a 100% return in a one-year period before the last of 2020’s bear market is rolled off later this month.

We chose an extreme time period to prove a point, but it is an important one for investors to remember. As the chart above shows, over short periods of time, the market has exhibited severe undulations, but as one stretches the time period, the variations become much smaller. For example, when looking at twelve-month rolling periods, the market has dropped more than 20% several times and gained greater than 40% a handful of times since the early 1990s. For five-year periods, the highs and lows moderate significantly, and over 10-year rolling periods, the market rarely has had a negative return but also has not posted annualized returns significantly over 20% for a decade in the modern era.

You may ask why we share this information with you now. The market has been favorable for a year and for the most part has trended upwards since the rebound from the Great Recession in 2008. But remember back 12 months, and you may not have been as optimistic about the market recovery. We do not blame you. It is stressful to look at your account when it is losing money. In the midst of a freefall, it is not easy to take a step back for perspective. Bear markets often happen when the world seems the most out of control. It feels right to do something, anything, to feel like you are in command. When that feeling occurs is when we suggest investors unplug and make no decisions of significance. Emotional decisions on either end of the risk spectrum can lead to regretful outcomes.

The period to plan for the next market reversal is now when markets are back near all-time highs, not after they have suffered significant losses. It is less mentally taxing to align your portfolio with your investment horizon when markets are strong. If you have already sat with us to review our capital market assumptions for the next decade, you have done the hard part of visualizing what poor capital markets can do to your portfolio. If you have not, consider how you would react to another drawdown like last year. Given enough time, it will happen again. If it took a team of horses to prevent you from reacting during the panic of last March, perhaps you consider making changes now, but what we have found is that investment portfolios can often weather market volatility better than the psyche of the investors responsible for them. If given the chance, the portfolio can recover losses over time. Time allows the miracle of compound interest to take hold and enhance wealth. If your current portfolio is aligned with your needs, the next time you find your stomach churning from the rollercoaster that is short-term market dynamics, you should mentally mosey on over to the treadmill of long-term results. It may not be as exhilarating, but it can keep you and your portfolio on a healthy path.

These articles may sometimes sound like broken records. Yet, some rules that are crucially important are also incredibly easy to forget under stress. If you would like to discuss your portfolio or know someone who would benefit from talking with us, we would welcome the conversation. We hope you are doing well and looking forward to Spring.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

Disclaimer Notice

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.