September 9, 2020

A friend asked me an interesting question the other day. “With interest rates so low right now, why do we care about the level of national debt? If we were paying 4% - 5% a year to borrow money, I would feel a lot worse than now when we are paying barely a tenth of that. Shouldn’t the current situation make it easier to pay off our borrowings?”

This article is not judging the need for the recent stimulus – we needed it. Instead the article is about long-term ramifications of debt if we do not develop a plan to mitigate its growth – or, perhaps, even pay it down. Theoretically, the last part of my friend’s question makes all the sense in the world… if the United States treated its debt like a home mortgage.

First, demographics and technological innovation are much different today than they were 20 years ago. The US has an aging population which tends to lead to lower growth and inflation rates as has been seen in Japan and Germany. Also, two decades ago, the internet was just starting to transform how we live, communicate and shop. It is now relatively mature, so it falls on robotics, artificial intelligence, or some other form of innovation to drive economic growth in the future.

Secondly, there is a buyer of new Treasury debt that brings with it enough purchasing power to keep a lot of this new supply off the market: the Federal Reserve. Since the Great Financial Crisis, the Federal Reserve has soaked up trillions of dollars of debt issued by the government. The Fed’s holdings of U.S. Treasury securities have increased from $2.2 trillion in August 2019 to $4.3 trillion as of August 2020. How do they do that? By printing money. So far, most of the money they have been printing has ended up in bank accounts, but what happens if the economy reopens with a boom rather than a whimper? Could inflation be on the horizon, pushing these low borrowing costs up?

If you look at certain assets (bond yields, gold, even Bitcoin) that typically go up in anticipation of inflation, recent market movements seem to indicate inflation expectations are increasing. However, we have seen false starts from these assets before. This could also be a classic liquidity trap where monetary policy fails to stimulate growth. Some folks we respect in this business say that we have been in such a liquidity trap since the Great Recession. Massive monetary stimulus has produced below historical trend growth and inflation.

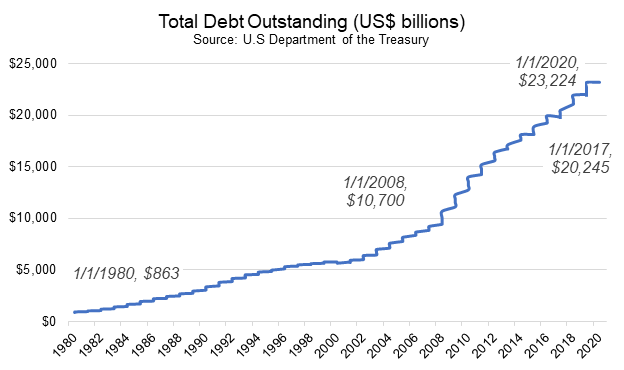

We have been monetizing a portion of our rising debt for years now. Over the coming decades, we will likely do the same as debt issuance moves from paying for crisis management to funding social and demographic related borrowing. As we sit here today, there seems to be little political appetite to get deficit spending under control.

We do not necessarily foresee short-term market implications of this massive borrowing. Things could remain on course for an extended period of time; however, at some point, if nothing changes, it is likely that either these borrowings will grow to a point where the market does not accept these low rates of return or inflation surges causing the Federal Reserve to remove some of its support for rates. The idea that tens of trillions of dollars’ worth of assets in tumult can end without issue seems a long shot to us.

So, to answer the question, right now, rates are low, and issuing debt should not keep my friend up at night, but his kids may want to hold onto their binkies a little longer.

1 Source: U.S Department of the Treasury Bureau of Fiscal Services

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.