April 23, 2020

“And up through the ground come a bubblin crude. Oil that is, black gold.” - Beverly Hillbillies Theme Song

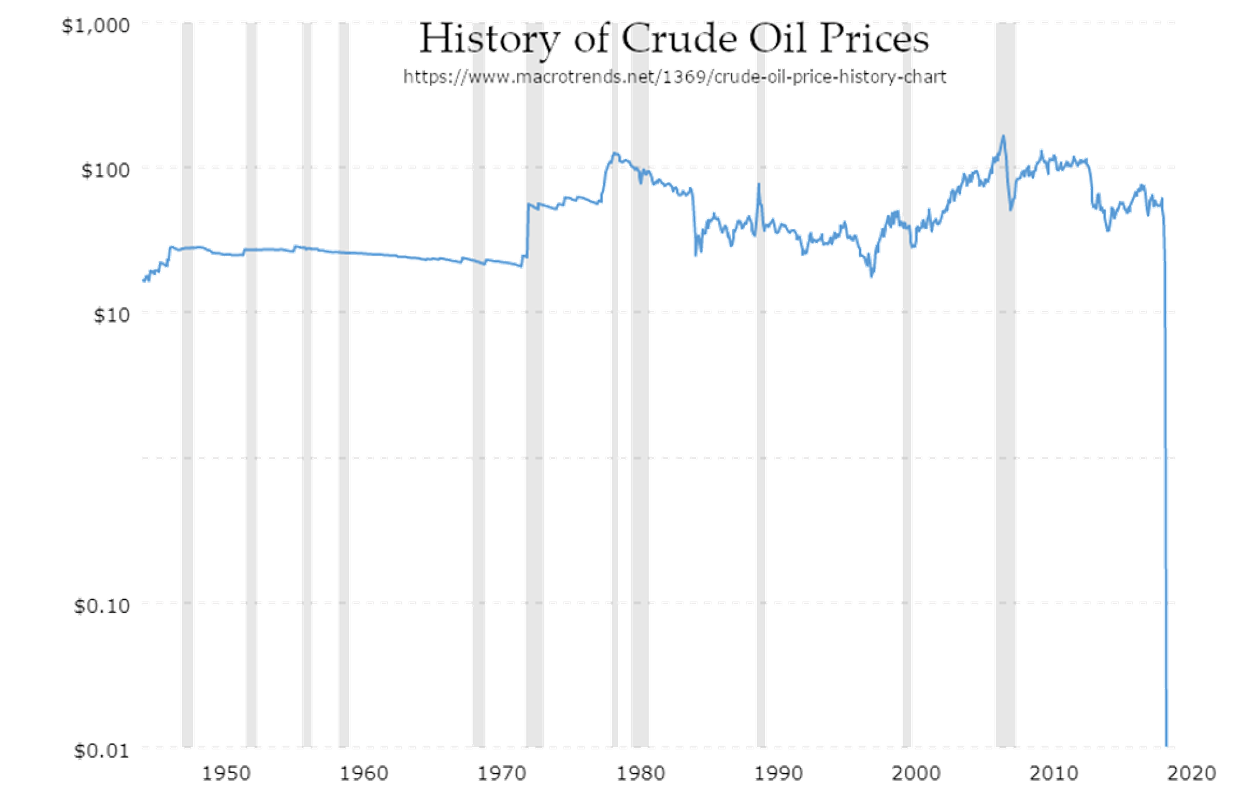

In college I had a buddy who told me that if oil was trading below $25/barrel he would get a job. If it was over that, he would sign up for graduate school. Cheap oil was a sign of a growing economy, whereas expensive crude put the breaks on global growth. I am quite certain that he did not have a game plan in the event of a barrel of West Texas Intermediate (“WTI”) oil costing negative $37 as it did this week.So, what happened? That Economics 101 course you have tried to forget came to life. Global demand for oil has plummeted with the COVID-19 economy – who needs gas when no one is travelling. At the same time, the global oil cartel headed by the Saudis and Russians fell apart, allowing oil to gush from the ground at a rate that was wholly unsustainable. Too much supply + too little demand + a lack of storage capacity = problems.

To be clear, oil, as a commodity, did not become less than worthless yesterday. Brent crude, which is a better grade of the black stuff and originates overseas, still costs money to purchase, albeit much less than a month ago. The phenomenon of WTI was that the May options contracts were expiring, and their mechanics dictate that the owner of the contract upon expiration must come to Cushing, Oklahoma and pick up 1,000 barrels of oil. Not many speculators have an appetite for that and thus chose to pay someone to take the contracts from them rather than finding storage for 42,000 gallons of crude.

As discussed in a previous edition, the Federal Reserve is unloading cash into the financial markets to provide liquidity where necessary. That the oil market “broke” (both figuratively and literally) and is not part of that Fed intervention should cause some pause for investors about getting too far away from their long-term plan and trying to pick up any “steals”. If the oil market’s performance could turn so anomalous without leverage, what could be the unintended consequences of $6 trillion of Fed driven cash on other markets? We stand by our long-held belief that things will be better in the future than they feel today, but we cannot stress enough that investors need to avoid self-inflicted wounds. Investors need to focus on allowing the power of compounding to do its job over time, a long time.

After an informal survey of my colleagues, we have concluded that making history in the investment business skews to the bizarre. Sure, you have some days where the stock market hits all-time highs but more often, when history is made, you get outcomes that hitherto would seem like pure gibberish. Oil trading below $0 certainly ranks up there with one of those. I wonder what my college friend is thinking right now.

We hope that you are all safe and healthy. We appreciate all of the support you have been providing us and hope that you feel the same. There was another issue of Independent Insights penned before the oil market went haywire. That can be found here.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

Disclaimer Notice

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.