November 23, 2020

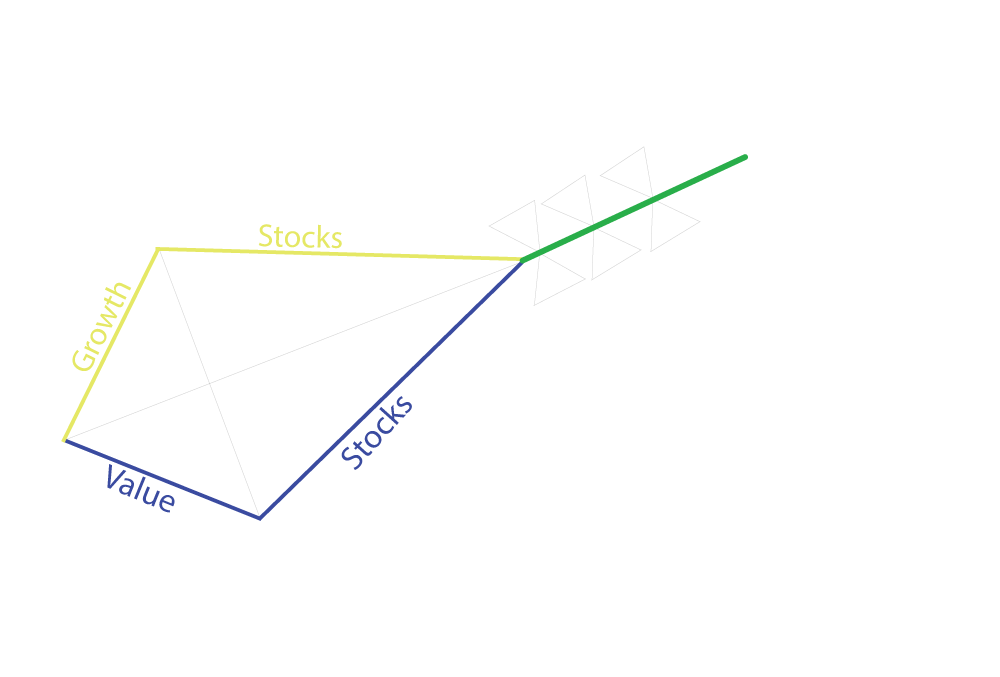

Well, the current situation could continue for some period of time, but at some point, a vaccine (or multiple vaccines) will be widely available, and we will return to some sense of normal we enjoyed before the virus. What then? Perhaps the proponents of the K are on to something but have not projected into the future. Could we see a Kite market where growth stocks continue to move higher, albeit at a more moderate pace, and value stocks lead the market by closing the gap that the pandemic created?

Economic recovery is the linchpin for value to show the recovery that is depicted above. 40% of the Russell 1000 Value is in financials, industrials, materials, and energy with about half of that weighting coming from financial stocks. A reopening obviously helps the latter three sectors which are directly correlated to the economy, but financials might be the most interesting piece of the equation. Stocks such as JPMorgan Chase & Co. (which has lost about 17% of its value so far this year as of the writing of this article) can benefit from three different levers of recovery. First, economic activity spurs loan growth. If companies

are more certain that the future is brighter than the present, they will borrow to fund growth. Second, financial companies have put billions of dollars into reserves for loan losses. If the banks have overestimated those losses, these reserves can become future profits. Finally, a rebound in the economy will likely cause the interest rate yield curve to steepen (longer rates will move higher more quickly than shorter interest rates.) When you are in the business of borrowing overnight and lending long-term (deposits versus mortgages, for example) steeper yield curves are profit centers.

The current price/earnings ratio on the Russell 1000 Growth is about 40x earnings. On the value index, the same metric is 17x earnings. These are based on profits over the past year. Growth proponents can jump up and down screaming that future expected earnings growth will accrete mostly to technology stocks rather than old economy equities. That could be true, but the high wire act of meeting those expectations can be tricky. From the value investor’s standpoint, it is hard to fall off the floor – unless of course, you have a basement.

If one believes that future stock appreciation will be muted, then dividends could become an increasing factor in returns. Growth stocks have historically paid paltry dividends compared to value issues. In large caps, value stocks currently pay about 4.5 times the dividends that growth stocks do. It has been years since dividends have been highly valued by market participants. Could lower return prospects and the potential for changes that even out the tax rates on income versus capital gains change that?

While we do believe that value and growth will converge – historically, they always have – a kite will not fly on a calm day. There is likely to be volatility and fits and starts to this coming together. During that time, investors should remain calmly at the helm. The kite may twist in unexpected directions as gusts blow across the sky, but subtle adjustments from the ground can help it stay aloft.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.