October 30, 2020

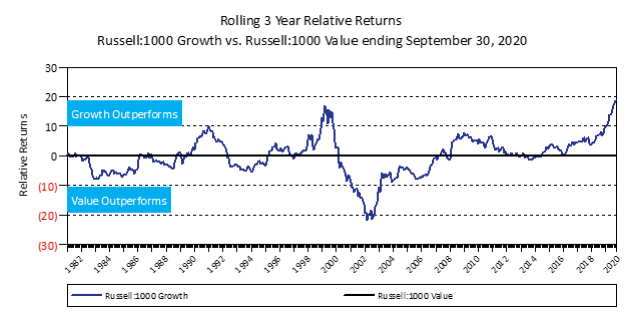

The chart below shows that over the last three years, large-cap growth stocks have outpaced large-cap value stocks by the largest margin since at least 1980. Only following the Tech Bubble bursting was there a greater divergence and that was in the opposite direction.

Going forward, will there be a repeat of these same tailwinds to drive growth further away from value or is this perhaps a situation in which Icarus is flying too close to the sun? Let us look at each of these three inputs.

Low interest rates – While the Federal Reserve has indicated that it intends to keep short interest rates near zero, it has also said that it does not want them going negative as has been seen in other areas of the world. Further out on the yield curve, where the Fed is less influential, interest rates have crept up from their lows in hopes of further stimulus followed by a COVID vaccine. Low interest rates support high price/earnings multiples1, and technology shares currently have robust valuations. Impact on growth stocks? – Our base case is that rates will stay relatively low for long but not drop significantly further. If this happens, the impact of rates on the prices of growth company shares should be neutral.

Profitability – This is one of the great unknowns. From an operating perspective, earnings should remain strong at these companies with low inflationary pressures on either commodities or employees. The flip side is that there exists a dark anti-trust cloud over these companies. The government has or is likely to file lawsuits against them since their dominance in various markets is clear. If the government (or any of the global regulators) acts aggressively to slow the growth of these companies, investors may punish them as they did following the 2001 Microsoft anti-trust case. Following those legal proceedings, Microsoft’s stock did not trade outside of a mid $20s – low $30s range until 2013. This was a lost decade for investors in the stock. Impact on growth stocks? – If legal issues gather steam, it could prove to be a strong headwind against profit growth for these companies which would be bad for share prices. If it fizzles, profits will likely remain robust and the companies should continue to gain market share either organically or through the acquisition of smaller competitors.

Pandemic – COVID-19 has been as problematic to value stocks as it has been beneficial to growth stocks. Because of the economic slowdown, banks are facing credit losses that have not been seen since the Great Recession2. Oil prices are down significantly on lower economic growth. However, in February and March, companies that were not yet able to support remote work had to kick spending into overdrive to outfit their offices, benefiting technology stocks. The question that growth investors should be asking is, “are there new revenue opportunities that haven’t been realized yet, regardless of the future of the pandemic?” It is hard to imagine a case where there are firms that have held out this long from equipping their employees, so it would seem to us that most of the gains in growth’s revenue streams have already been realized. Impact on growth stocks? – Companies that rely on cloud-based revenue for their growth will need to find new avenues to meet investor expectations. If expected growth rates begin to slow, it may be difficult for the market to continue to sustain such high valuations for these stocks.

If history has taught us anything, it is not to bet too heavily on any one outcome. There are factors not covered here that one could consider to make a strong bull or bear case for growth versus value; however, what nature has taught us is that no tree grows to the sky. As of this writing, Apple, Microsoft, and Amazon make up almost 30% of the Russell 1000 Growth Index which makes us feel less diversified than is usually the case when holding an index position. At some point, the economy will change and with it the current stock market darlings. We do not know for sure when that will happen, nor do we know the exact reason why it will, but we are confident that it will.

We hope you and your families are doing well. Please do not hesitate to reach out to discuss any of these thoughts.

[1] For more information on this, please see our most recent Independent Insights "Time Value of Money".

[2] https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/us-loan-loss-reserves-approach-great-financial-crisis-levels-60310921

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.