March 30, 2020

“Oh, he might have gone on living, but he made one fatal slip

When he tried to match the ranger with the big iron on his hip.”

- “Big Iron” lyrics by Marty Robbins

There is an epic battle raging right now between the Federal Reserve and investors to maintain order in the mortgage backed securities (“MBS”) market. If this was Ali-Frazier, it wouldn’t be the “Thrilla in Manila”, but it might be the “Trillas for Villas” since the Fed has committed trillions of dollars to promote liquidity across the fixed income markets with a special focus on housing.Before we get into what is happening these days, let us begin by describing the combatants, the importance of the playing field, and why you should care about the outcome.

In one corner, we have the Federal Reserve, the 90-year reigning champ of these battles. With the mandate of full employment and controlled inflation, the Fed enters the ring with the ability to print infinite amounts of money to achieve its goals. Its one deficiency is that it is not empowered to put capital at risk in the use of its quantitative easing goals, and therefore, must rely on the Treasury Department to backstop some of these operations.

In the other corner, we have fear-induced illiquidity. Illiquidity has often challenged the Fed in times such as these and has been beaten back, but it is a formidable foe. It lurks in the dark and springs forth unannounced, often when things seem the best and our attention is elsewhere. Like 2008, illiquidity brings with it to the ring its tag-team partner, the threat of massive defaults in the housing market due to a slowing economy.

Today, the two combatants square off in pitched battle over an incredibly important piece of turf: the housing market. When you buy a home, sometimes the bank holds your mortgage, but often, they want to sell it to be able to recycle those dollars for more loans. Fannie Mae and Freddie Mac exist to purchase those loans and package them together for investors in the form of MBS. The investors earn income as you repay your loan with Fannie and Freddie, who provide guarantees against loss in case of a default. In terms or returns and risk, MBS usually fall between Treasury bonds and corporate bonds. They normally pay a bit more than Treasury bonds but also do not normally face the same volatility corporate bonds do.

As of the end of 2019, there was a total of $10.3 trillion of MBS outstanding, trailing only Treasury securities which total $16.7 trillion.* Failure of MBS would not only freeze the housing market (which accounts for somewhere between 10% - 15% of gross domestic product), but it would also cause losses for investors from the big Wall Street Banks to the small IRA you may have tucked away somewhere. To boot, the Fed is hoping lower borrowing rates will allow people to refinance their current mortgages and in turn utilize some of those savings to help kickstart the economy when everyone is free to socialize and spend as desired. MBS are ubiquitous.

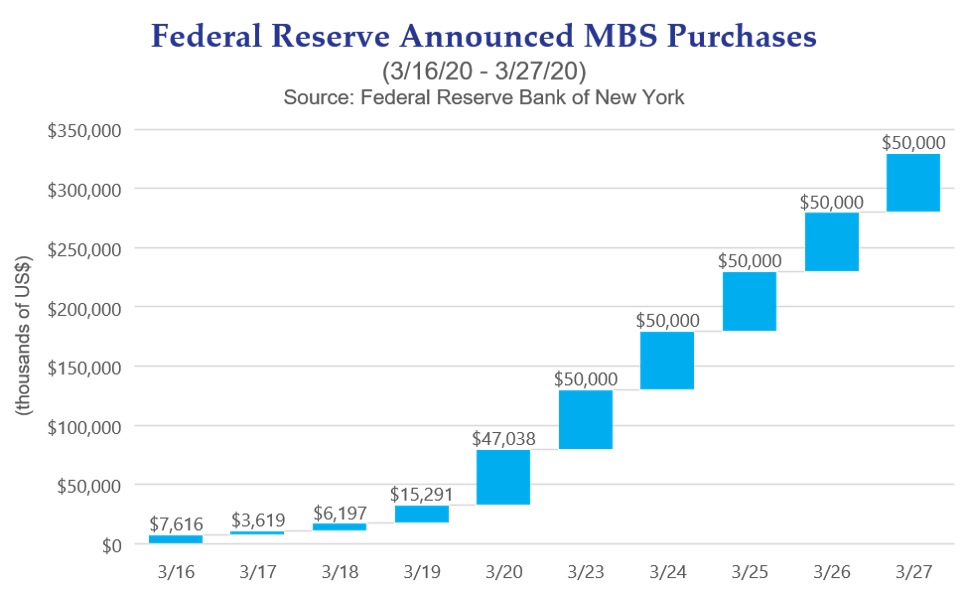

Clearly, the Federal Reserve has a vested interest in making sure this market functions smoothly. It has come to the rescue in prior times of stress, and recently it announced an unlimited amount of firepower to try and quell the current upheaval in the market. The sheriff is coming into town to take on the illiquidity outlaw. The chart below shows the announced schedule of purchases; we expect there to be as many dollars aimed at the problem as necessary until it is resolved. The Fed, indeed, has a big iron on its hip.

Will the Fed maintain its championship belt? Our experience is that fighting the Fed is a losing battle; however, as mentioned above, the Fed is not allowed to lose money. If it is in a position to purchase risky assets, the Treasury Department must backstop it. One of the fears currently in the market is that if borrowers cannot make their payments because they cannot work, then there may be a wave of defaults which would spread harm onto the banking system. Given the work that has gone into propping up this economy by both the Fed as well as the federal government, this outcome is not our base case, but it is certainly something we will be reviewing closely.

To mix metaphors one more time, we do believe that once the sheriff has time – and calming this market will take time – we will find illiquidity bandit lying flat, or more likely vanquished to the shadows waiting for another opportunity to strike.

We will make it through this and hope that you and your families are taking care of yourselves. Cornerstone remains open for business, so do not hesitate to get in contact with us. We look forward to being able to see you all soon and will keep you informed of what we are thinking.

*According to the Securities Industry and Financial Markets Association website (www.sifma.org)

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

Disclaimer Notice

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.