September 18, 2020

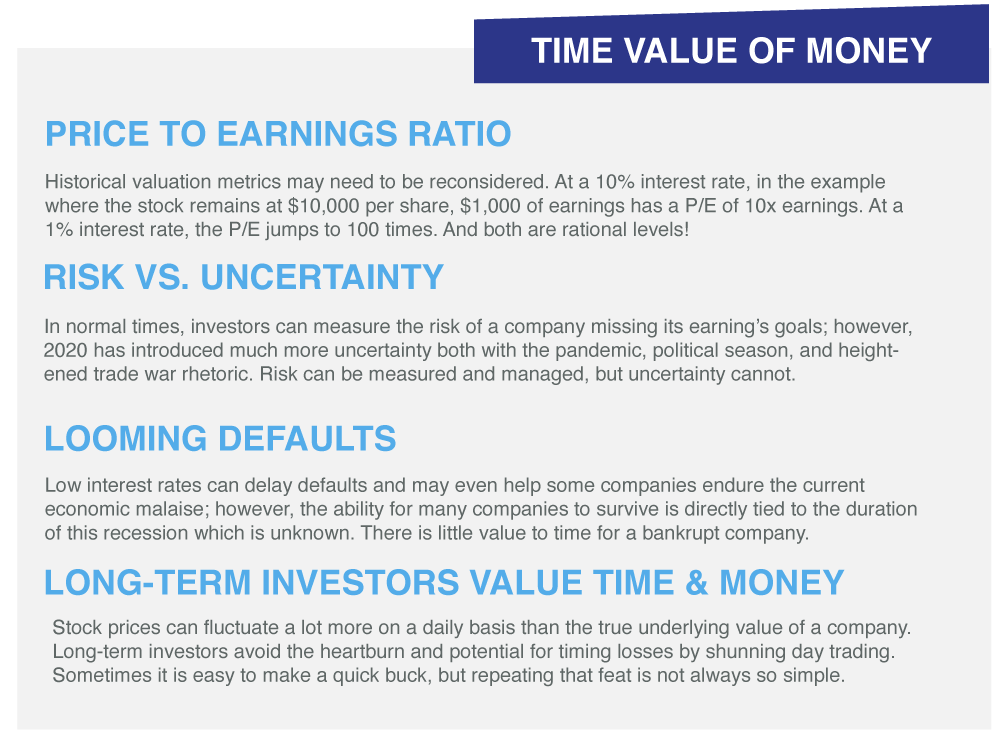

This concept ties perfectly into today’s world where there seems to be a disconnect between the real economy’s struggles and the stock market’s boom. If earnings’ expectations fall, so too must stock prices, right? Not necessarily. Stock prices can be thought of as the present value of a company’s future expected earnings. For our purposes, dividends will be considered part of those earnings, and we will ignore other metrics such as free cash flow. Given that stocks, unlike bonds, are expected to provide investors with an eternal share of a corporation’s earnings, we use the formula for a perpetuity (Price = Earnings/Interest Rate) to value shares. Starting with an extreme example, if a company’s earnings are $1,000 per year and interest rates are 10% per annum, an investor should value the stock at $10,000 ($1,000/10%). If nothing changes except for a drop in the interest rate to 1%, the stock value jumps to $100,000 ($1,000/1%). Our investor just earned 10 times his initial investment solely because rates dropped! Conversely, to maintain the same $10,000 per share value in the interest rate decrease scenario, earnings could drop 90% - to $100 per share, and the price would not change.

We all know that the example above is an excessive one, but since the beginning of the year, the 30-year Treasury Bond yield has declined from 2.4% to around 1.3% today. In other words, earnings expectations would have to drop by more than 46% in the future for the market to be valued less than it was heading into 2020.

One caveat to the above is that interest rates are not the only input into this equation. If those low-interest rates fail to spur economic growth, earnings may come in lower than expected, swamping the rate cut effect. In all times there are going to be arguments for and against higher equity valuations. Sometimes the market is overly dour, sometimes too exuberant. Depending on who you talk to, there are even times when the market is both! Do not latch on to one story and do not fixate on one metric. Doing so will likely mean you miss the big picture.

We do not see the current runup in technology shares approaching either the South Sea or even the Tech Bubble of the late 1990s, but anytime we see stocks appreciate at a fever pitch, we want to take a step back and look at whether the fundamentals support the thesis.

At the end of the day, no one knows for sure where the market is heading over the coming weeks and months, but what we do know is that the market recovery has been a sight to behold but not totally unwarranted. As we have said before and will say forevermore, it is best to revisit your portfolio’s asset allocation from a position of strength rather than during times of stress. If you have any questions about that, please reach out to us.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.