February 25, 2020

Treasury bond yields react to two main inputs: economic growth and inflation expectations. As either ticks up, so do rates; however, threats to either can have the opposite effect, pushing rates down. The current risk to global economic growth posed by the coronavirus is a prime example, driving the 10-year Treasury bond yield from about 1.9% to start the year to 1.4% now.

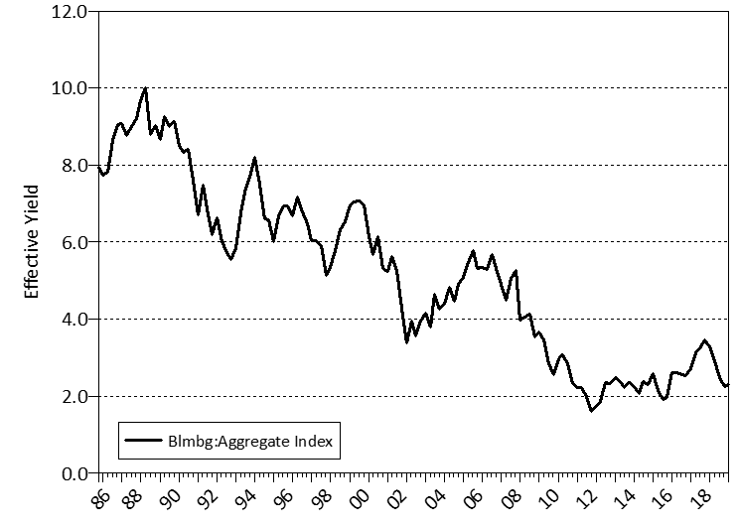

However, this article is not about the short-term gyrations of the bond market; it is about the implications that low interest rates pose for long-term return expectations. As you can see below, the yield of the Bloomberg Aggregate Index has been in steady decline since the mid-1980s. Whereas investors used to be able to buy fixed income securities and reap a yield of 8% - 10%, the current expectation for interest income from high quality fixed income is only in the 2% range. This puts a lot of stress on risk assets to provide investors with the returns to which they have become accustomed.

Most institutions have a targeted return of 7.5% to avoid invading the principal of their portfolios. Not-for-profits spend around 5% of their endowments annually with the other 2.5% of growth aimed at meeting inflation. Over the long run, a simple 60% stock/40% bond portfolio has achieved that goal fairly consistently. Because of the dismal outlook for fixed income going forward, many current capital market assumptions indicate that investors would need to put almost all of their money in risky assets to achieve that 7.5% target return. Of course, making such a drastic move into stocks meaningfully increases the magnitude of losses in the event of a market downturn.

If an investor cannot tolerate the volatility of an aggressive portfolio in search of the desired return, are things hopeless? Not necessarily. We often advocate one of two solutions for clients feeling despair in the face of lower expected returns. First, no one’s crystal ball about the future of the markets is clear. Many things happen along the way that move these expectations in unknown ways. In light of that, investors can acknowledge that for some period of time, they may modestly underperform their targeted return while avoiding the possibility of a massive drawdown that is inherent in a very risky portfolio. If the forecasted returns turn out to be too conservative, a 7.5% rate of return is not hard to achieve. If the forecasted returns are correct, a slight erosion of capital may occur. Neither outcome seems like the end of the world.

The second solution is to consider constraining liabilities (i.e. spending) given lower asset growth expectations. Most people would agree that it would be imprudent to budget more spending in a year than you are expected to earn. Why, then, would it be rational to keep spending at a rate that worked in the past but is unlikely to work going forward? We understand that spending cuts are painful, but they are sometimes necessary. Given the market’s strength over the last decade, now might be the right time to look at that belt tightening versus waiting for the next downturn.

The above example focused on endowments, but the potential solutions exist for all investors. Maybe public funds contribute more than their minimum requirement? Maybe participants in 401(k) plans increase their savings to offset lower expected returns? These are the conversations that all investors should be having.

We wish you all the best and thank you for your continued readership.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.