June 16, 2022

That supply problem is a CURSE (China, Ukraine-Russia, and Strong Employment.) In fact, the Global Supply Chain Pressure Index2 is extremely elevated and not showing signs of an imminent easing.

China – China is a manufacturing powerhouse, accounting for almost 30% of total global aggregate production, according to the World Bank. The country’s industrial output is 1.7 times that of the United States, its closest competitor. When the country entered into its Zero COVID lockdowns, upwards of $10 billion per day of goods were not produced. The impact of $10 billion dollars of lost output, in normal times, may be a rounding error of global GDP; however, a significant portion of Chinese industrial output is in electronic component parts rather than finished goods. The lack of these “parts” has a ripple effect around the world on final goods output from smartphones, to cars, to washing machines and beyond.

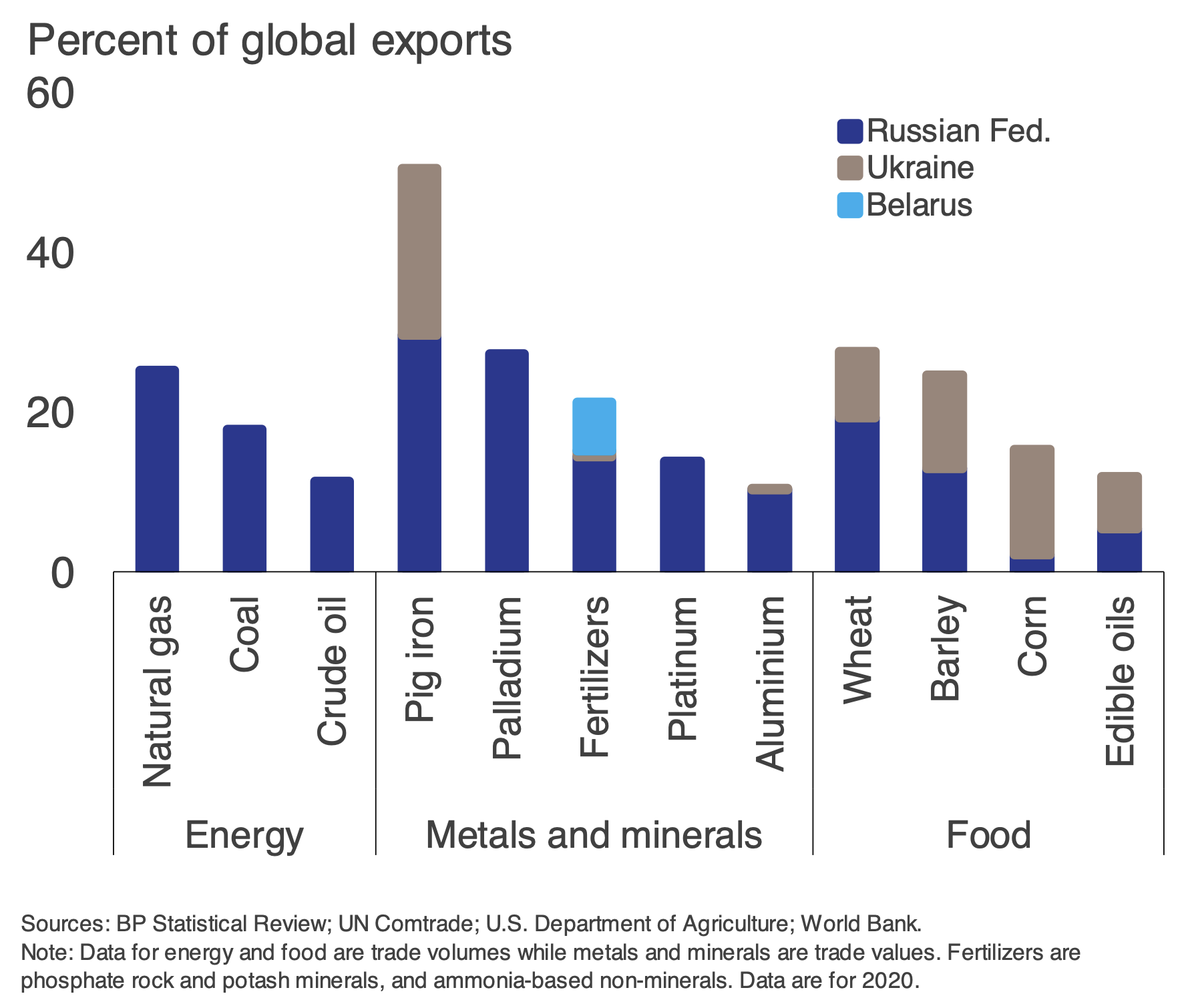

Ukraine-Russia – Russia is most certainly a key exporter of oil and natural gas, but upwards of 25% of the world’s fertilizers, wheat and barley, not to speak of corn and iron, have effectively been cut off from global markets due to Russia’s invasion of Ukraine. Again, like the Chinese component issues, taking this production offline inflicts widespread economic damage both directly and indirectly and requires the supply chain to change in less efficient ways to deliver goods where they are needed.

Strong Employment – Theoretically, the shortages caused by foreign shocks could be solved by the economic might of the United States; however, we need time and workers to do so. Given the low unemployment in the country, we do not have significant underutilized resources that can be brought online quickly. There are not enough idle workers that could be employed to fill the gaps created overseas, nor can US manufacturing be expanded overnight. The current manufacturing capacity utilization readings show that we are at the sustainable maximum output given our current stock of factories. Strong employment is usually a desirable economic trait, but not a limitless one.

Without fiscal alternatives (not that they do not exist, just that they are unlikely), that leaves the Federal Reserve to fight rapidly increasing costs. The Fed is wonderful at providing and removing liquidity from the economy. They can pluck the chords of consumer demand like Yo-Yo Ma playing the cello. Supply issues, however, are the Fed’s kryptonite. Monetary policy cannot pump more oil, grow more grain, or build an iPhone. They can raise 50 basis points, they can raise 1%. The only effect that they can have on inflation in an environment like this is to squash demand, which is not oversized, to fit the supply that we have and likely create a recession. Land wars in Asia rarely come without a lot of misery.

The potential good news is that the financial markets are forward looking. They do not wait for economic developments to occur; they often move in anticipation of such events. We expect heightened volatility to continue for some time given the multitude of issues happening in the world, but we also remind investors that the time to plan for times like these are before they happen rather than in the midst of them.

1 Real Personal Consumption Expenditures as tracked by the U.S. Bureau of Economic Analysis, https://fred.stlouisfed.org/series/PCEC96

2 Federal Reserve Bank of New York, Global Supply Chain Pressure Index, https://www.newyorkfed.org/research/policy/gscpi#/interactive

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

Disclaimer Notice

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.