August 22, 2019

The year is 2012.

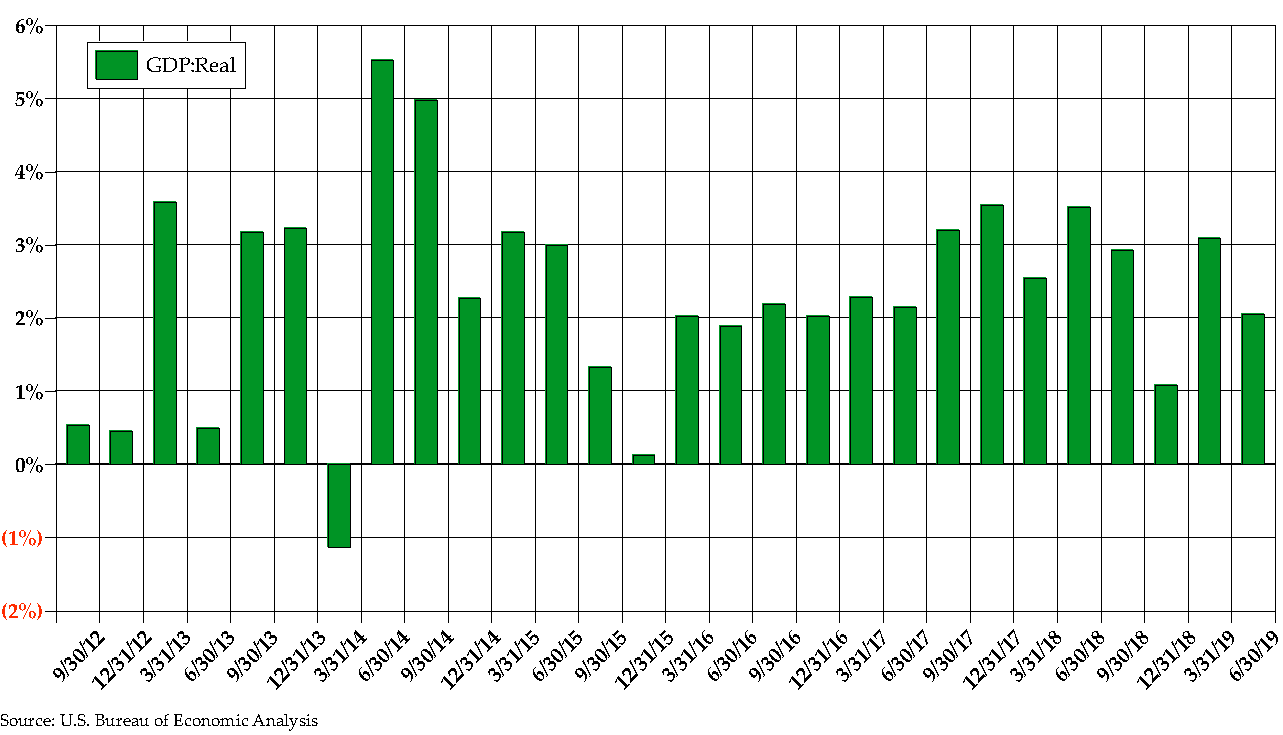

On September 13, 2012 the Federal Reserve delivered in a big way, unleashing Quantitative Easing 3 onto the nonbelievers of the economic recovery. This serving of monetary stimulus propelled the S&P 500 upwards by 14% per year (from July 1, 2012 through June 30, 2019), and as the chart below indicates, the broader economy found its footing soon thereafter.

Fast forward to today and many similarities exist, but so do some differences. We too wait for the Fed’s next move; however, we are embroiled in a trade war with China, an economic drag that did not exist 7 years ago. Another, and perhaps more important, difference between then and now is that the yield curve has inverted, and trillions of dollars of debt globally have negative yields. Neither statistic can be construed as a positive outlook on future growth.

What is interesting is that commentators speak as though the yield curve is a sentient force acting on its own, rather than a collection of market participants expressing their views of future economic growth. Absent significant global supply gluts or serious financial stress – we would argue that neither situation currently exists – an inverted yield curve can signal a loss of confidence. Uncertain monetary and fiscal policy cause companies to lose faith in their ability to forecast sales into the future. When this happens, these firms tighten their spending with spillover effects occurring up and down the supply chain. If the negative sentiment is not contained quickly, self-fulfilling prophesy can take hold, causing a real-world recession.

We do not know for certain if history is or is not repeating itself right now. It certainly is humming a familiar tune. What we do believe is that there is no underlying reason for a recession in the near term other than unnerved markets. If the Fed can manage the market’s expectations without triggering inflation, and the trade wars are contained, we may be seeing 2012 all over again. If any portion of this solution fails to instill confidence back into the real economy, then a recession in the not too distant future is not off the table. There can always be something: a stellar earnings season, great jobs numbers, an unexpected intervention by an overseas central bank, or any other glimmer of hope that provides a jolt of confidence the market needs. These would be welcome relief for a while, but until the tariff situation and uncertainty around Fed policy become more benign, it is hard to believe that we have seen the last of the volatility that has been upon us since July turned to into August.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.