August 7, 2019

“And you better gird your loins, buster. You got a fight on your hands.” - Barney Fife

It should not have come as a surprise that China just weaponized its currency, the yuan. The escalating trade war of tariffs, broken promises, and hurt feelings promised to turn one-sided on September 1st when another round of tariffs on Chinese imports is put into place. The purpose of currency devaluation is to mitigate the effects of tariffs on exporters. The Chinese just do not import enough from the U.S. to go dollar-for-dollar in that arena, so weakening the yuan was their main avenue of recourse, with the cut to agricultural purchases from the United States a politically-aimed smart bomb. We leave to political scientists the discussion of the risks posed by decreasing globalization to America’s global hegemony, but what we do know is that international trade is not a zero-sum game. More trade creates more wealth and helps developing economies thrive while providing developed nations with cheaper goods. Less trade leads to lower standards of living for everyone.

As we have mentioned several times previously, the global economy has been able to withstand short-term disruptions caused by this trade war; however, there is a stark possibility that both the U.S. and China are playing the long game. Could the Chinese be resigned to some short-term pain in hopes of regime change in the U.S. in 2020? Our economic situation has yet to show obvious stress, which may allow the administration to continue its current course as well.

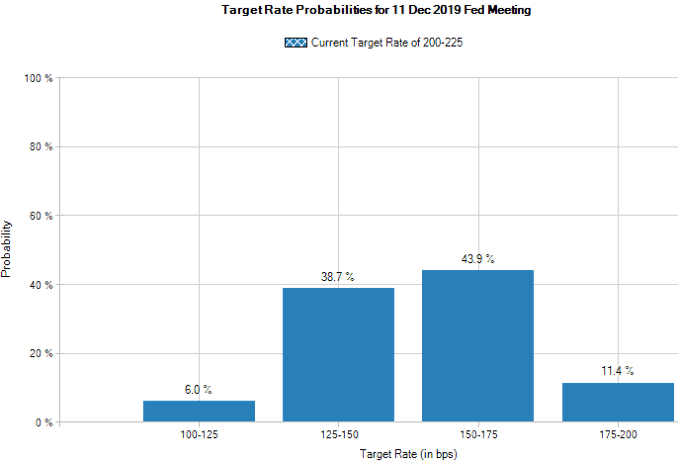

What may happen if this trade spat begins harming the real economy? Our guess is that the Federal Reserve will need to continue its decade-long Lone Ranger routine and ride to the rescue again. As the chart below shows, courtesy of the CME Group[1], the market is putting a 100% probability of at least one rate cut before December and an almost 50% probability of 3 or 4 rate cuts.

Being a central banker is hard enough in peacetime but navigating a $90 trillion global economy through these self-inflicted tribulations seems nearly impossible. Central banks in New Zealand, India, and Thailand have already made surprise cuts to interest rates. Given the slow growth the world is currently experiencing, more central banks will follow suit to protect their domestic economies. Tepid growth and low interest rates combine to magnify monetary missteps; there is not a lot of space for central banks to course-correct if they deem it necessary.

While we still think that following the lead of the Fed and ignoring the noise of the trade dispute has merit, we also understand that there may turn out to be some weaknesses in that strategy if resolution does not come soon and escalation continues. Hope is not a strategy for success, but it does not mean that we should not wish fervently for a resolution to the trade issues before things get bad. As always, we will keep you abreast of information as it becomes available.

[1] You can track these probabilities in real time at https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

Disclaimer Notice

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.