May 29, 2019

“I’m in debt. I am a true American.” - Balki Bartokomous

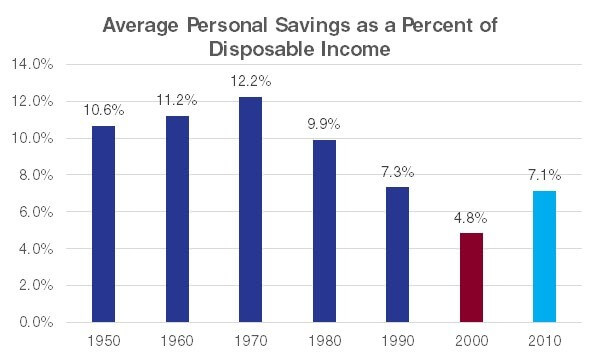

Back in the late 1980s and early 1990s, Americans thought they borrowed too much, as evidenced by the above quote from Perfect Strangers (a tragically underrated comedy). From 1986 through 1993, when the show was in its original run, average personal savings rates as a percent of disposable income in the United States[1] was 8.5% per year. In retrospect, America has not been as frugal since those “spendthrift” days.

It is not surprising that savings have rebounded since the debt-fueled 2000s. Many households, once burned by excessive borrowing, have retrenched and are no longer living on the proverbial edge. Saving more may be a good thing for individual families, but it is not always so for the general economy. We all understand that savings, in general, are good, so let us focus on why the global economy needs the American consumer to spend rather than save.

Let’s start with the expenditure model of calculating gross domestic product:

GDP = Consumption + Government Expenditure + Investment + Net Exports

Globally, net exports zero out, and investment refers to businesses building machinery, buying plants, etc., not investing in the stock market. If one assumes that companies do not invest without demand, the two key determinants of economic growth are therefore consumption and government expenditures. In the US, government spending is about one-third of the size of consumer spending and is offset largely by tax revenue, which mutes its economic impact. This allows us to focus just on consumption as a core driver of economic growth.

The last memory of Eco 101 that we will dredge up is that there are only two choices of what to do with your money – you can either spend it or save it. As illustrated above, Americans save about $0.07 for every dollar earned. Globally, savings rates are above 25%, with the world’s second largest economy, China, experiencing personal savings rates above 47%[2].This global savings glut is both culturally and economically driven, meaning that it is unlikely to change quickly. The growing middle class in China should help mitigate its bloated savings rate over time; however, this is a generational issue, meaning that the American consumer is likely needed to drive economic growth for the foreseeable future.

To give you a sense of the impact our domestic consumers have on the world, consider that a 1% decrease in the savings rate would increase spending by almost $150 billion per year, increasing our own GDP by 0.7% and global growth by 0.2%, not to mention the knock-on effects coming from increased corporate expenditures. In a low growth environment, these numbers are significant.

We are not advocating for you to max out your credit card, but we do think that the impact the consumer has on economic growth is an important indicator for investors to track.

We hope you had a wonderful Memorial Day, and we extend our thanks to all of you who are currently serving or have served our country in the past.

[1] As measured by the Bureau of Economic Analysis.

[2] World Bank Group data as of 2017.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

Disclaimer Notice

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.