October 3, 2019

At Cornerstone, we manage a robust private client business consisting primarily of entrepreneurs. For those of you who are entrepreneurs or know one, you understand that they are constantly in transition. Whether it is expanding the business, looking at intergenerational transfer of ownership, or an outright sale of the business, the landscape is forever changing. Entrepreneurs tend to work in their businesses more than on their businesses. They understand what makes their companies successful but sometimes fail to make sure that more mundane aspects such as buy-sell agreements are up to date.

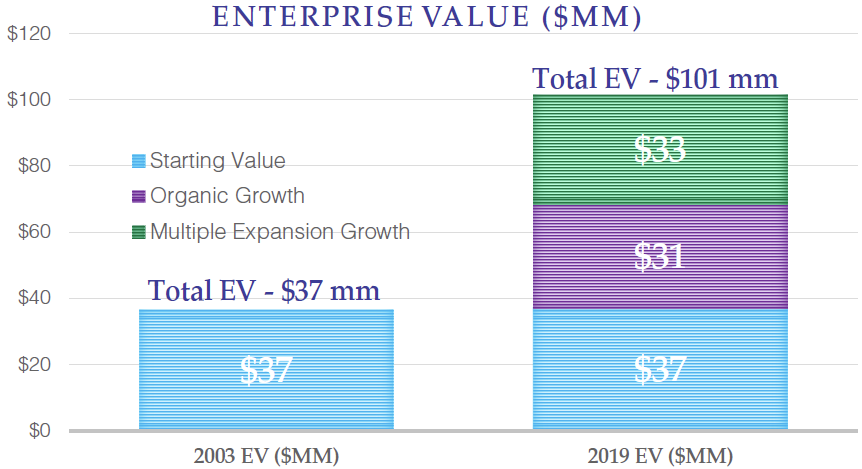

How do the prior two paragraphs tie together? For one, there is a lot of money looking for a place to be invested, and secondly, that pot of money includes trillions aimed towards buying companies that are privately held. The chart below utilizes information from Bain & Company[2]. Imagine that in 2003 you made your last visit to your business advisor. At the time, you had a company that made $5 mm annually in EBITDA (earnings before interest, taxes, depreciation and amortization), which is a metric commonly used to value a company. In 2003, the private equity market would have paid you 7.3x those earnings for your company, or a total of $37 mm. From 2003 until 2019, the economy grew by about 86%, so let’s assume your company’s earnings grew by that amount. That would have added another $31 mm to its value, but instead of the market paying 7.3x for your now $9.3 mm of EBITDA, private equity firms were offering, on average, 10.9x those earning. You now have a company worth over $101 mm!

A business that grew like this would have to be considered a success story, right? Not necessarily. Remember, in this example, you last updated your business documents in 2003. That means you likely planned and financed a buy-sell agreement[3] that is more than $60 mm short of what is necessary to pay market value. What happens if a 50% owner of the business passes away? It appears there is a financing gap. Again, in this case, the entrepreneur worked in the business more than on the business; that success, alongside a lack of planning and funding, may force the remaining shareholders to take unwanted calls from private equity firms since the current owners cannot afford to purchase the shares of their deceased partner.

On a related note, we would suggest you revisit your business plan with your advisors even if you have no interest in selling or have not had the type of increased valuation described above. The recent tax law changes allow for intergenerational gifting in amounts not previously afforded. These gifting changes are not permanent and could be overturned as soon as next year’s election.

As always, we thank you for taking the time to read this Independent Insights and wish you a healthy and happy fall!

[1] https://www.preqin.com/insights/blogs/alternatives-in-2019-private-capital-dry-powder-reaches-2tn/25289

[2] Bain & Company Global Private Equity Report 2019

[3] An agreement between shareholders/partners dictating the method and value for purchasing one another’s shares.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.