October 15, 2019

For investors with a proclivity towards trend investing, this has led to an interesting dichotomy. Some want to increase their international exposure while others are asking why they should own these underperforming assets at all. Let us look at scenarios in which those who are bullish on international stocks could win out in the long run. The opposite outcomes would likely continue the winning streak of domestically leaning investors.

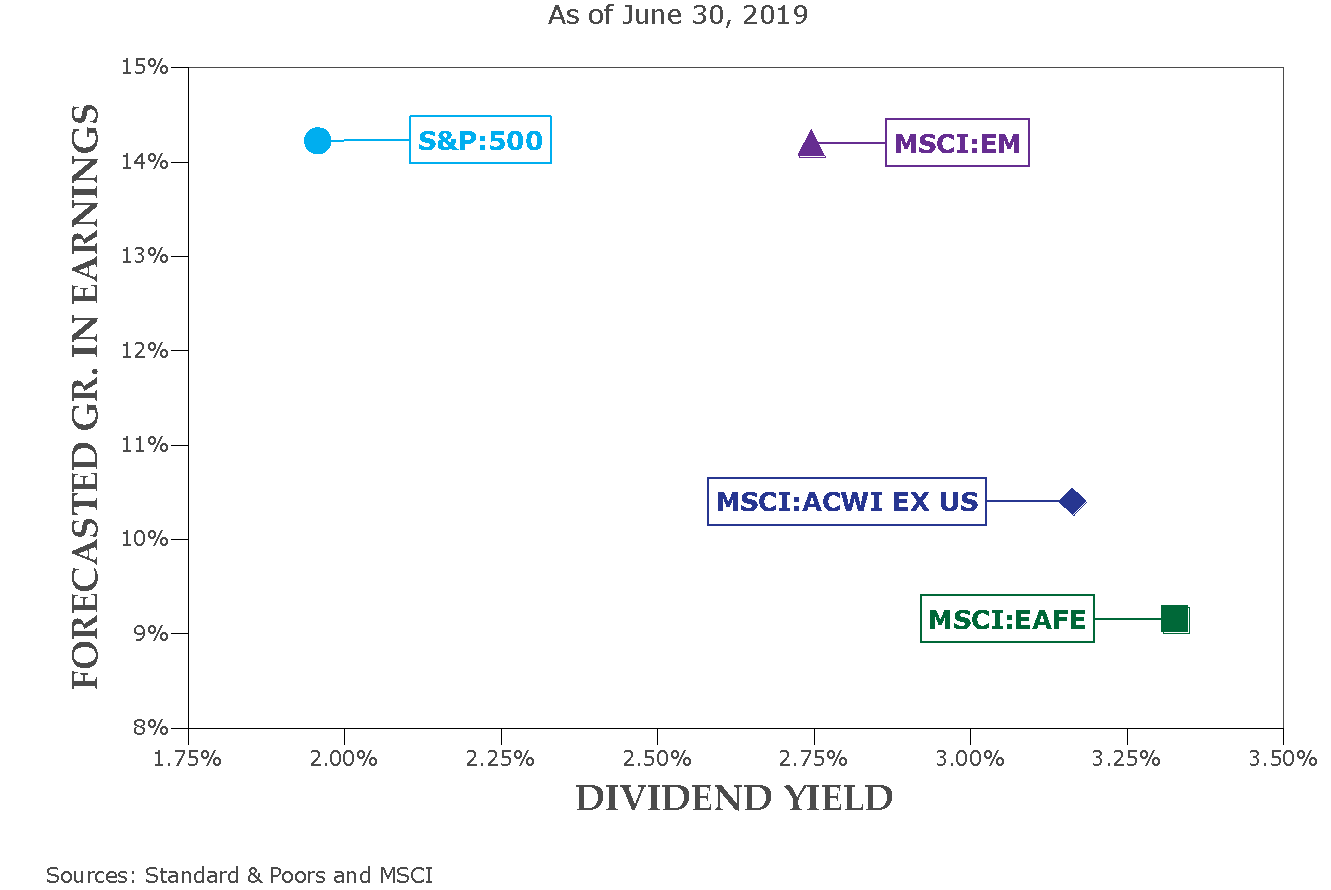

An Earnings Recession – if companies globally fail to produce the level of earnings growth that the market is predicting, the S&P 500 is starting with higher expectations and thus has further to fall. The price/earnings ratio of the S&P 500 is also elevated compared to the MSCI EAFE.

A Global Recession – the trade wars and a lack of confidence may have already triggered certain countries into recession and appear to have caused a manufacturing recession. If a loss of confidence triggers a global recession (more of our thoughts on this can be found in our August 22, 2019 issue of Independent Insights) the elevated level of dividends outside the US could make those stocks look attractive, assuming the recession is shallow, and those dividends are stable.

A Rejection of US Treasury Issuance – to date, the uncertainty of the global landscape and the vast quantities of negative yielding bonds globally have made for relatively smooth funding of the US’s $1 trillion annual deficit. There have been no repercussions to this irresponsible fiscal management. Yet. If that changes, and it can change on a dime, interest rates could quickly bounce from record lows, pressuring companies with high outstanding debt.

A Resolution of Geopolitical Problems – if the reader thinks the US political situation is a mess, look overseas. Europe is locked in the Brexit abyss, China has significant debt and growth issues, the Middle East is eternally on the brink, etc. If the shadows being cast by these overhangs recede, one could see a path to international stocks outperforming over the coming decade.

The Federal Reserve Diverges – each time the Fed signals that is will raise rates (or even hold steady), the market for risk assets quivers. To date, the Fed has capitulated. Foreign central banks are much more comfortable being accommodative, given more tenuous economic growth, than the Fed. What would happen if the Fed finally came through with significant tightening of monetary policy while the rest of the world continued easing? Theoretically, the dollar would strengthen, giving a boost to foreign economies through increased imports into the United States. If that move turned out to be significant, it could go a long way to bolster foreign economies and ultimately their stock markets.

There are a lot of reasons to be concerned about international stocks, which is why we generally maintain an underweight to them compared to what GDP or market capitalization levels would imply. It would be easy to say that the quality of US stocks is higher than those of international stocks, which is why they trade at a higher valuation. However, as Mr. Bogle points out, at some point markets tend to revert to the mean and valuation dispersions close. What he was wise enough to avoid in his quote was the speed at which reversion happens or the triggering event. At some point, the international bulls will be correct, but from our vantage point, it may take a while.

*When comparing the returns of the S&P 500 (U.S. large cap stocks) with the MSCI EAFE (developed international stocks) for one decade ending 09/30/2019.

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.