September 14, 2021

Inflation, a word which for decades has been an afterthought, is being discussed quite a bit nowadays. The last time this nine-letter word generated so much debate was during the oil crisis of the 1970s. Currently in developed countries, such as the United States, inflation remains stable and low. The annualized inflation for the United States for the past decade has fallen short of the Federal Reserve’s target rate of 2% per year. Since inflation has languished, much more talk over the past generation has been geared towards the second of the Fed’s mandates: the unemployment rate. During times of economic tumult, the insidious effect of rising prices does not grab headlines like people who have lost their jobs.

Due to deliberate actions taken by the Fed and Congress in response to the COVID-19 crisis, the economy received much needed support and has seemingly got back on track. Monetary authorities loosened policy by dropping interest rates, buying securities, and implementing a lending strategy to stimulate the economy. Congress acted swiftly by distributing stimulus checks, unemployment benefits, and supporting businesses. These actions achieved two main objectives: keeping the economic wheels turning and providing support to those most affected by the lockdowns.

A year ago, the main concern was getting the economy stabilized, which, in hindsight, was achieved. According to the Bureau of Labor Statistics, unemployment has fallen from a peak of 14.8% in April 2020 to 5.2% in August 2021 and barring any further nasty coronavirus surprises continues to trend in the right direction. Although full employment has not yet been achieved, when does the Fed change its focus to rising prices?

Combining an economy that appears to be growing with a Fed Funds rate of 0.25% could certainly lead people to wonder if this is too good to be true. All this liquidity in the economy has helped the financial markets, but it is also creating some knock-on issues, with the prime one we hear being, “Why is everything so expensive suddenly?” From groceries to automobiles (both new and used) to the surge in home prices, price increases have left some consumers flabbergasted.

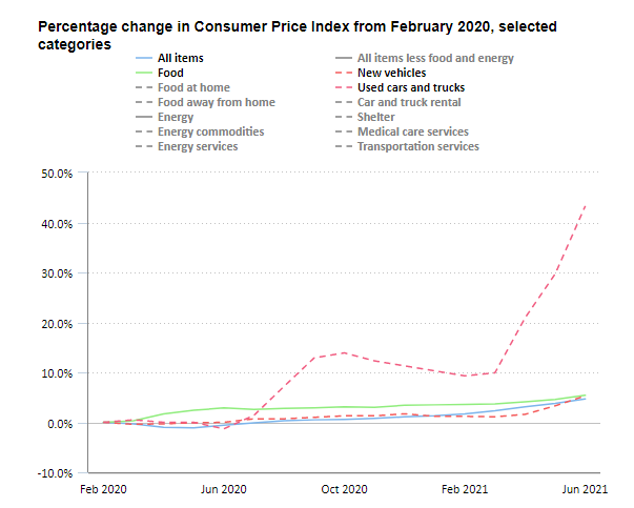

Both the Fed and the markets are pricing in transitory inflation: prices are high right now but should trend back to normal over the coming years. One example is that the increase in automobile prices is being driven by a global microchip shortage (you might be surprised by how much our supply chain in all areas relies on these little silicon wafers) and that rental car companies have needed to restock their fleets which they sold off during the initial phases of the lockdown at the same time production has slowed. Home prices have surged in the last year as well; driven by a combination of people moving out to the suburbs due to new work from home policies, and reduced interest rates. Although far from ideal, theoretically these price shocks will eventually subside as new vehicles are produced, and people return to the office.

The chart above shows the levels of inflation for: all items, food, new vehicles, and used cars and trucks from February 2020 to June 2021.

We believe that the Fed is closely looking at its impact on inflation, but fiscal policy is also a large contributor to potential inflation as a lot of stimulus has been passed in the last year. With a $1 trillion infrastructure bill (to give you an idea of how much money $1 trillion is, it is about $3,000 for every person in the United States) and a potential $3.5 trillion budget reconciliation bill on the horizon, fiscal spending has been extraordinary.

Loose monetary policy and enormous government spending are accelerators of inflation; however, there are some important decelerators that need to be considered. New variants of the coronavirus are a disruptive threat to economic growth. Whether through government mandate or just consumers showing hesitancy to reenter their pre-pandemic spending patterns, an overheating economy is not a forgone conclusion.

Something to remember is that news is coming out every day that can cause investors to lose focus on the long-term. It is important to digest this information without overweighting the newest, most fantastic data being published. The price of lumber, which doubled year-over-year several months ago, has plummeted back to pre-pandemic levels. Why? People cut more trees down to meet the market needs. We do not believe that the inflation toothpaste is out of the tube at this point, but if fiscal and monetary authorities squeeze too hard, the work of getting it back to acceptable levels will not be enjoyable for anyone.

Mihir serves as Project Manager, Asset Management at Cornerstone and joined the company in 2021. Mihir is primarily responsible for portfolio management, investment due diligence, coordinating long-term corporate initiatives, and serves as a support for the CIO. He is also a member of the Innovation, Investment Policy, and Marketing Committees. Mihir earned a master’s degree in Corporate Finance and a Management Consulting Certification at the Pennsylvania State University, Smeal College of Business. He received a bachelor’s degree in Economics and a minor in Business Administration from Millersville University, where he served as CFO for the Marauder Fund, a student investment association. In his free time, Mihir enjoys playing tennis, cooking, and spending time outdoors.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.