July 9, 2019

“It is not the beauty of a building you should look at; it’s the construction of the foundation that will stand the test of time.” - David Allan Coe

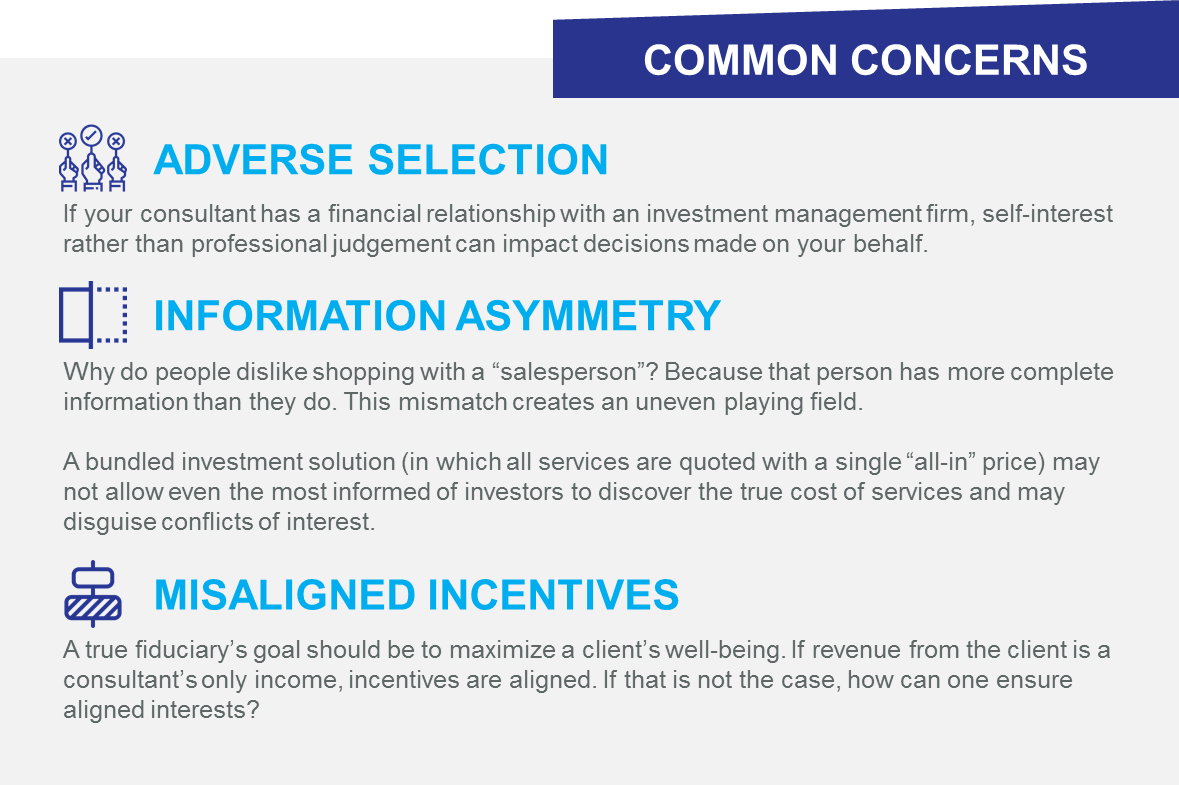

I am an unrepentant game theory nerd. I have been accused of thinking in its terms and am at it again. In the most recent “View from the Corner Office” our CEO, Tom Scalici wrote about open architecture and the importance of having an independent consultant to guide your investment program. In an upcoming issue of Network Magazine, my colleague, Chris Lakatosh, discusses why you should have an advisor willing to take fiduciary responsibility for your assets[1]. In this Independent Insights, we synthesize the two and discuss why fiduciary standards and open architecture are important.First, let us consider some definitions. Different pools of assets have differing governing regulations, such as ERISA, the Uniform Prudent Management of Institutional Funds Act, Pennsylvania Fiduciary Statutes, and others, but they all have a commonality: duty of loyalty. That allegiance requires those in a position of trust to put beneficiary needs above their own self-interest. Open architecture, although used loosely in the investment industry, means a fiduciary can engage any qualified firm, without restriction, to serve a client. A fiduciary adhering to a truly open architecture investment solution lays a foundation for trust by avoiding three pitfalls common to our industry:

These three issues are at the heart of the “Principal-Agent Dilemma,” which is one of my favorite game theory problems. In short, it is your money, but you need to hire someone to manage it since you do not have the specialized skill required. The hired person/firm has the specialized skill but does not own the assets, and therefore their goals may not always be aligned with yours. There may be outside factors influencing his or her decision-making.

So, what to do? If you cannot move to a true open architecture platform, the game theory solution is to change the precepts of the relationship in one of two ways. The first is to hire another professional whose only compensation comes directly from you. That third party can monitor the activities of a bundled solution provider on your behalf. The second method is to contractually require your advisor to fully disclose compensation from third parties. Neither solution is particularly efficient, nor do they address the heart of the problem.

We are firm believers in open architecture as the superior strategy to mute the Principal-Agent dilemma. Unfortunately, fiduciary law has not codified it as such; the rules allow companies to serve multiple roles in investment programs. The conflicts inherent in these solutions melt away when each provider independently serves only you. Any excess fees or malfeasance by one party will negatively impact the others, ensuring alignment of interests between you and those who serve you.

For those who wish to go it alone, the Securities and Exchange Commission does require registered investment advisors to disclose conflicts in their Form ADVs; however, despite recent attempts at creating user-friendly disclosures, the industry lingo found therein can be difficult to decipher to most laypeople.

Bundling your home and auto insurance may yield economies of scale, but that may not be the case with your investment solution. Partnering with an independent, open architecture co-fiduciary lays the foundation for peace of mind knowing that your advisor is working solely on your behalf.

[1] If you wish to receive a copy of either, please reply to this email or reach out to loyalty@cornerstone-companies.com

Kevin is Cornerstone’s Chief Investment Officer and is involved with the firm’s Investment Policy and Strategic Planning committees. Kevin joined the company in 2000 after graduating from Lehigh University with a B.S. and M.S. in Economics and earned his CFA charter in 2005. Kevin supports many charitable causes and has established a donor advised fund to propagate his philanthropic interests. Kevin lives in Bethlehem with his cats Zola and Charlyne, enjoys woodworking, gardening, reading and travel. Kevin is the proud uncle to many nieces and nephews and loves spending time with and spoiling them.

Disclaimer Notice

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.

This material is prepared by Cornerstone Advisors Asset Management, LLC (“Cornerstone”) and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the published date indicated on the article and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Cornerstone to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Cornerstone, its officers, employees or agents. This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Any accounting or tax advice contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.

The information is provided solely for informational purposes and therefore should not be considered an offer to buy or sell a security. Except as otherwise required by law, Cornerstone shall not be responsible for any trading decisions or damages or other losses resulting from this information, data, analyses or opinions or their use. Please read any prospectus carefully before investing.